Retail Resilience 2026: Turning disruption into competitive advantage

10 minute read

How resilient retailers turn disruption into competitive advantage

Research with 129 senior retail executives, 2,000 UK consumers and the annual reports of 30 major retailers reveals how risk, AI and new growth channels are reshaping strategy in 2026.

UK retail is entering a more demanding phase in which disruption is broader, more connected and harder to contain. Cyber threats, cost pressure, platform dependency and shifting customer behaviour are converging, while AI, international markets, social commerce, retail media and circular models are creating new routes to growth. In this environment, resilience is moving beyond protection from risk to become a source of agility, relevance and competitive advantage.

What you can learn from this report

• How to benchmark business readiness across the seven pillars of retail resilience.

• How connected risks can move across operations, finance, strategy and reputation at the same time.

• How AI-led discovery is changing brand visibility and the path to purchase.

• How to evaluate international growth, partnerships and emerging trading channels without losing commercial control.

• How to turn resilience into board-level indicators, faster decisions and stronger demand sensing.

Key report insights

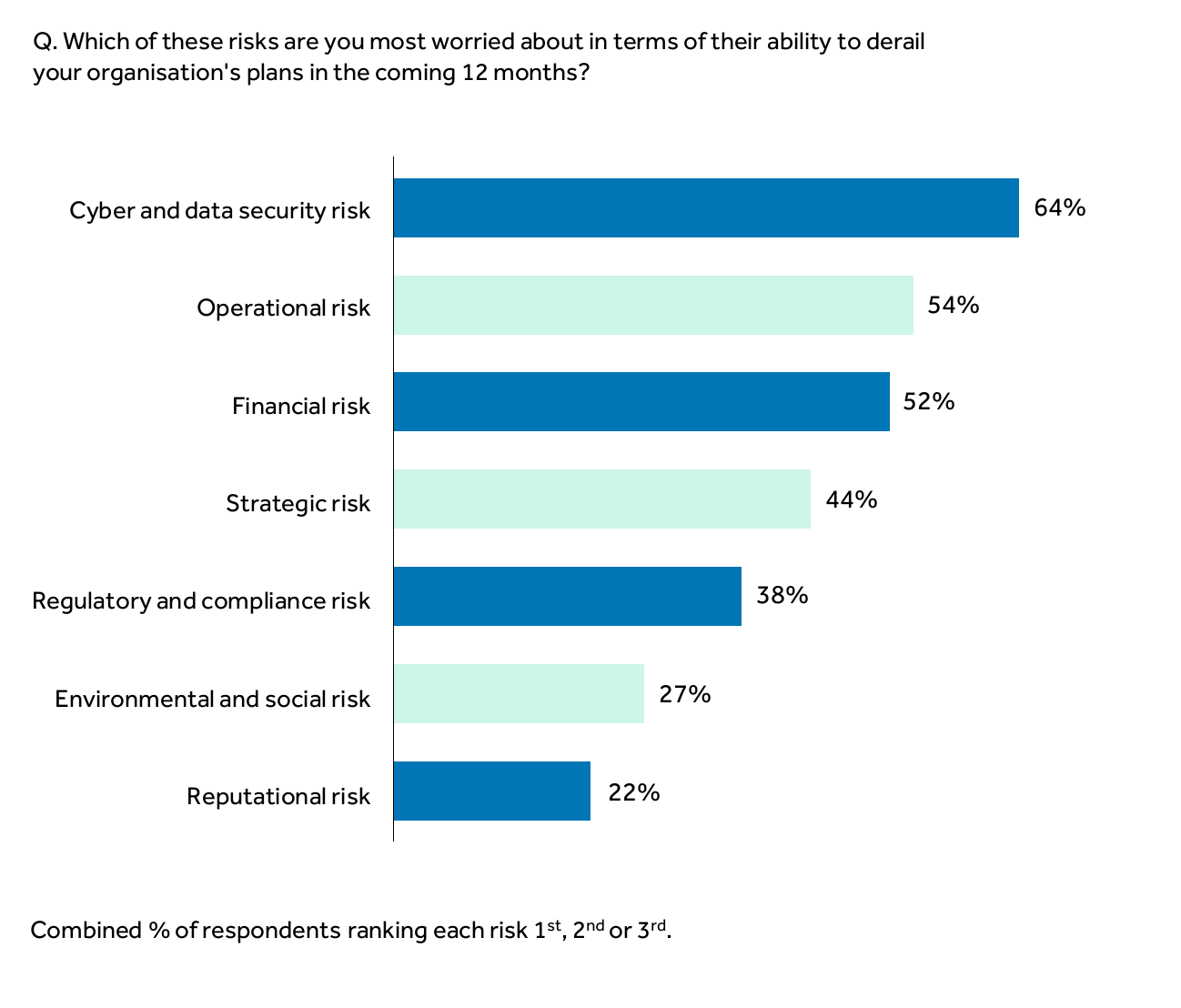

• 64% of retail leaders place cyber and data security among their top three risks, up from 58% in 2025 and ahead of operational risk at 54% and financial risk at 52%.

• 37% of retailers rate themselves as highly prepared for a possible cyberattack, up from 25% a year earlier.

• Strategic risk is now a top-three priority for 44% of leaders, rising from 42% in 2025 and 34% in 2024.

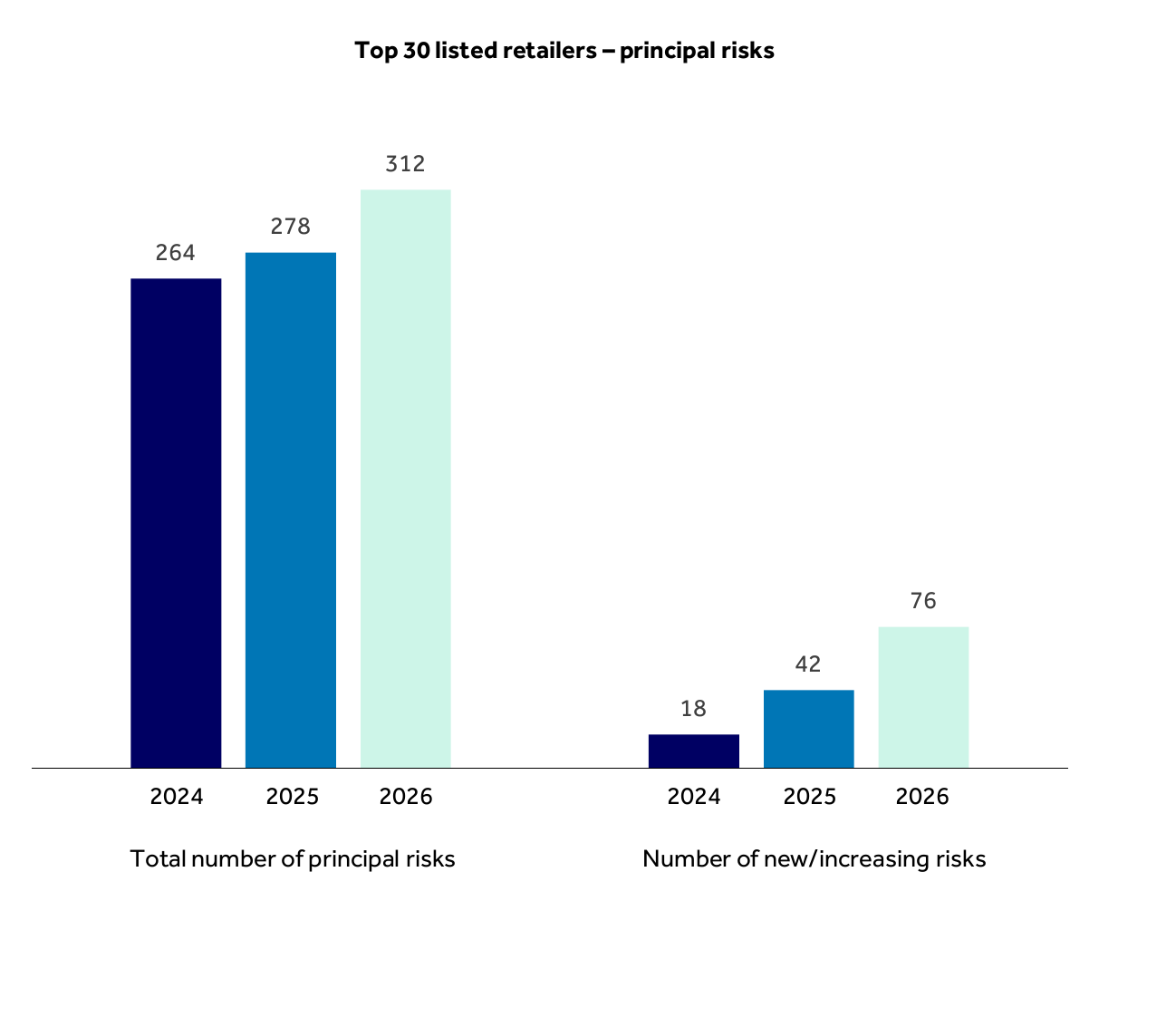

• The top 30 listed retailers disclosed 312 principal risks in 2026, while the number classified as new or increasing climbed to 76 from 42 in 2025 and 18 in 2024.

• 70% of UK consumers have used conversational AI in the past year and 38% have used it for shopping tasks; 78% of retailers agree AI is already reshaping discovery.

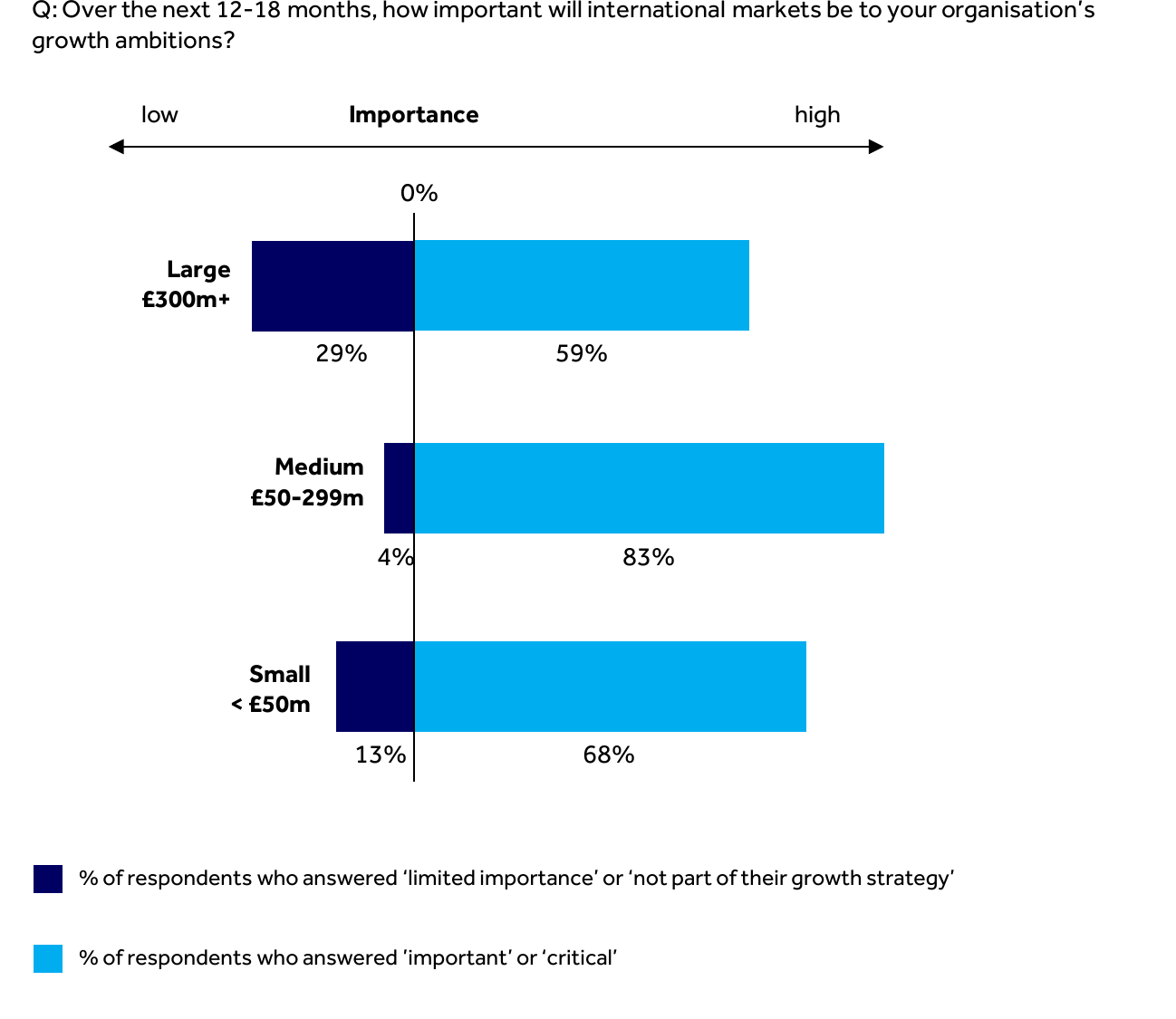

• 74% of retail leaders say international markets are important to growth, rising to 83% among medium-sized businesses.

• 30% of Gen Z shoppers have recently purchased through TikTok Shop, while the UK social commerce market is forecast to more than double from £9bn in 2025 to £20bn by 2030.

A connected framework for resilience

Retailers are moving from managing individual risks in isolation towards responding to a broader set of overlapping pressures across the business. The Retail Resilience Framework assesses readiness across cyber and data, operational, financial, strategic, regulatory, reputational and environmental resilience. Strong leadership and organisational culture underpin every pillar.

Retailers are operating in a market that is constantly evolving and increasingly shaped by sustained, overlapping pressures. In recent years, successive waves of disruption from cost inflation, supply chain instability and rapid technological change have compounded, reshaping the operating environment. Many have adapted, but resilience is now being tested in more continuous and demanding ways.

Figure 1 – Retail resilience framework

Source: Retail Economics, Barclays

*Barclays provides financial services to a range of sectors including high-emitting industries such as oil and gas. We’re working to reduce the emissions we finance and support clients in the transition; for more information visit: home.barclays/climatechange

Cyber risk returns to the top

Cyber and data security has returned to the top of the resilience hierarchy, with 64% of leaders placing it among their core focus areas. The shift reflects a growing recognition that cyber is not a standalone IT issue, but a commercial risk capable of halting trading, disrupting operations and eroding customer trust. Although preparedness has improved, the scale and sophistication of threats continue to evolve.

Board focus has broadened. More than two-thirds of retailers now report increased attention across eight of the eleven risk areas we track, most rising 10 to 20 percentage points on 2025. Cybersecurity (81%) and technology and digital disruption (80%) lead. Only regulatory and compliance change has eased.

Figure 2 – cyber security has solidified its position at the top of retailers’ biggest concerns for the year ahead, and is now also first choice risk

Source: Retail Economics, Barclays

Operational and strategic pressures dominate escalation

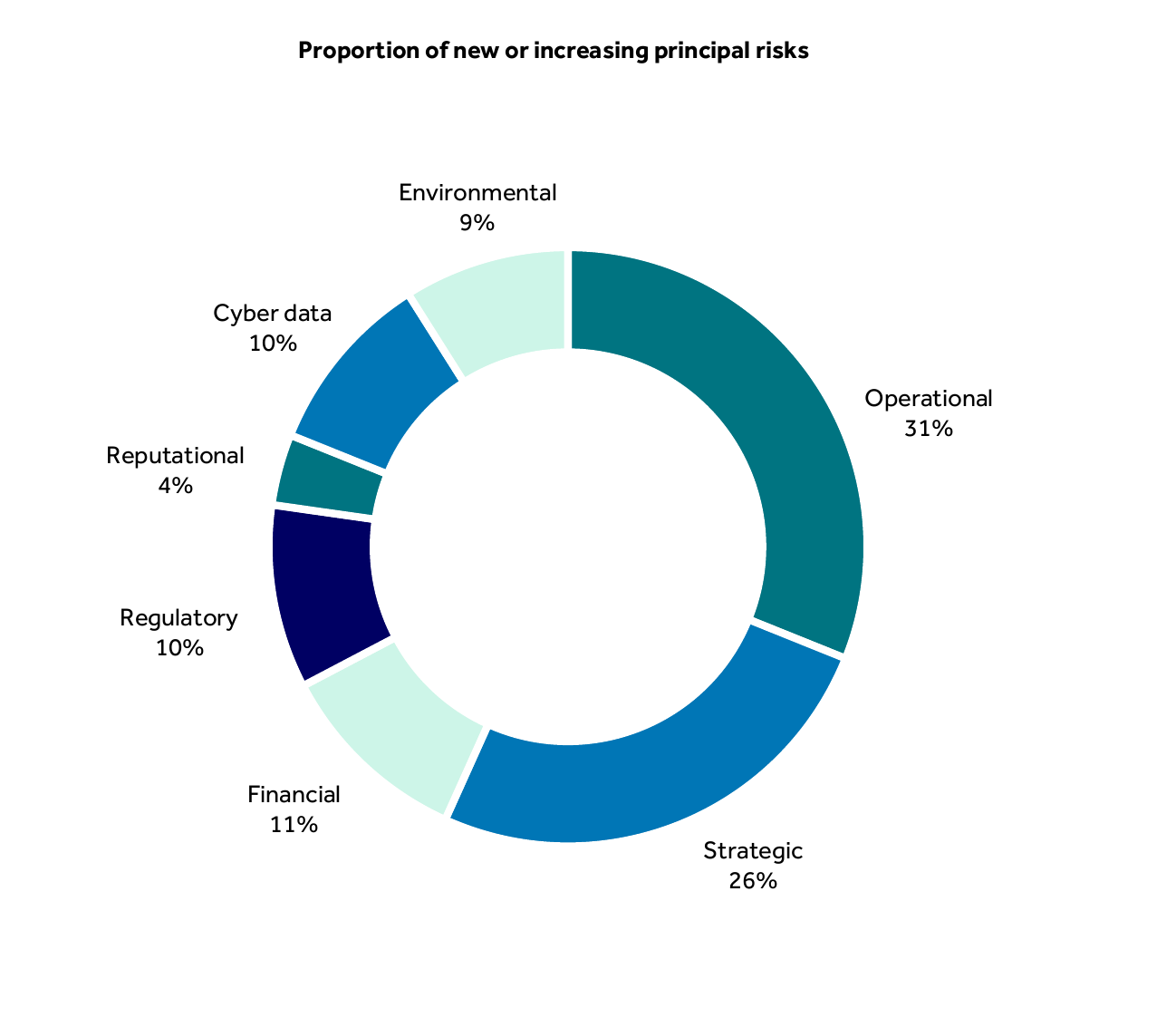

A review of principal risk disclosures from the top 30 listed UK retailers shows that pressure is neither easing nor narrowing. Operational risks account for 31% of all new or increasing principal risks and strategic risks account for a further 26%. Boards are increasingly focused on whether business models, supply chains and decision-making structures are fit for a less predictable market.

The customer journey is becoming more fragmented. Consumers move across a wider set of touchpoints, from social platforms and marketplaces to mobile apps and physical stores, with expectations around value, convenience and experience continuing to rise. AI is starting to reshape how products are discovered and evaluated, changing how retailers need to show up and compete for attention.

Figure 3 – principal risk disclosures rise as retailers look to strengthen resilience

Source: Retail Economics, Barclays

Resilience is becoming a performance capability

The total number of principal risks disclosed by the top 30 listed retailers has risen from 264 in 2024 to 312 in 2026. Over the same period, risks described as new or increasing have climbed from 18 to 76. Resilience is therefore becoming harder to separate from performance, shaping how effectively businesses protect operations, adapt to change and position for growth.

Retailers are moving from siloed responses to joined-up strategies. Resilience is increasingly defined by the ability to adapt at speed as multiple pressures converge. With margins under pressure, businesses have less room to absorb disruption, and boards are under growing pressure to show how a wider set of risks is being managed.

Figure 4 – principal risk disclosures rise as retailers look to strengthen resilience

Source: Retail Economics, Barclays

Growth abroad creates opportunity and complexity

International expansion is becoming an important way to offset weaker growth at home, particularly for medium-sized businesses. It offers access to new pools of demand, supported by rising ecommerce penetration and growing middle-class consumption in high-growth markets. However, it also requires stronger capabilities in sourcing, fulfilment, pricing, working capital, compliance and local execution.

International growth is becoming a more important part of the retail playbook. At the same time, overseas competition is becoming harder to ignore at home. For many businesses, this is creating a more complex balance of trade: looking abroad for new demand while defending market share and margins in a more competitive UK market. Ongoing geopolitical uncertainty and global conflict add an additional layer of consideration for retailers, who must carefully consider instability when exploring where to expand internationally.

Internationalisation brings its own resilience demands. It requires stronger capabilities in sourcing, fulfilment, pricing, working capital, compliance and local market execution. Done well, it diversifies growth and reduces dependence on the UK market. Done poorly, it adds complexity at exactly the wrong moment.

Figure 7 – the importance of international markets to growth, by business size

Source: Retail Economics, Barclays

Spotting weak signals early means combining customer, trading and operational data to track behaviour changes as they emerge, whether driven by AI-led discovery, social commerce, overseas competition or GLP-1s. The advantage comes from responding faster. This includes adjusting ranges, pricing, marketing and inventory early enough to capture growth and stay ahead of shifting demand.

The retailers most likely to outperform will combine sharper commercial judgement with stronger operational discipline. That means investing in the right capabilities, building flexibility into decision-making and responding early to changes in demand. In 2026, resilience is evolving from the ability to absorb shocks into an active competitive capability that helps retailers defend margins, stay relevant and create the conditions for sustainable growth.

Download the full report to explore all five resilience themes and the strategic actions retailers can take in 2026.

About this report

This report was produced by Retail Economics in partnership with Barclays Corporate Banking. The analysis draws on a survey of 129 senior retail executives conducted in April 2026, economic modelling and insights from the annual reports of 30 of the UK’s largest retailers, and a nationally representative survey of 2,000 UK consumers exploring shopping behaviour, AI-led discovery, social commerce and emerging health trends. All analysis was conducted by Retail Economics.