UK Retail and Leisure Outlook Report 2026

DOWNLOAD FREE REPORT

3 minute read

DOWNLOAD FREE REPORT

The 2026 outlook: How retail and leisure leaders can turn uncertainty into profitable growth

Download your FREE preview version now, and we'll email you the final report as soon as it's published so you don't miss out!

Important note: The content on this page is a preview only. It is designed to signal the areas of focus explored in the full outlook and does not include final research, statistics or quantified findings. The full report will be published shortly.

UK retail and leisure enters 2026 with opportunity still on the table, but with far less margin for error. Cost pressures remain embedded, consumers are spending with more scrutiny, and competitive intensity continues to punish weak propositions and slow execution. This preview sets out the agenda for our forthcoming UK retail and leisure outlook report, highlighting the core themes and strategic questions that will define the year ahead.

What you can learn from this outlook report

- How the sector’s margin environment is evolving, and what execution-led performance looks like when pricing power is constrained

- The key shifts in consumer behaviour moving from cutbacks to cautious, deliberate spending, and what this means for volume, mix and loyalty

- The consumer trends likely to shape 2026, including the changing role of online, the rise of circular behaviours, and the pressures reshaping value perceptions

- How retailers and leisure operators can adapt to disruption by rewiring customer journeys, sharpening propositions and defending margin through targeted investment

- A practical playbook that brings the themes together into clear priorities for profitable growth in 2026

Questions brands should be asking in 2026

Senior teams can use the outlook framework to pressure-test plans, align trading assumptions and focus investment. The themes in the report are designed to help leaders answer a set of practical questions that are becoming unavoidable in 2026:

- Where is demand proving resilient, and where is it still constrained by affordability, caution and trade-offs

- What parts of the cost base are structurally higher, and which levers offer real productivity gains without degrading experience

- How should propositions evolve when value is judged across price, quality, convenience, reliability and trust, not price alone

- How should online and store roles evolve as social commerce, cross-border disruptors and AI-led discovery reshape journeys

- Where should investment be prioritised to protect margin while improving conversion, service quality and loyalty

Key insights

• The turbulence of recent years has eased, but the conditions created have become structural, requiring businesses to adapt rather than wait for a rebound.

• Growth in 2026 is expected to be modest, with real GDP forecast between 1% and 1.5%, reflecting continued drag from fiscal consolidation and polarised consumer spending.

• Peak inflation has passed, but price pressures remain sticky, continuing to weigh on real spending power.

• Margin pressure remains intense, driven by labour costs, business rates and regulatory change, reinforcing the need for disciplined cost control.

• Financially resilient and digitally fluent households are driving spending, increasingly influenced by AI-shaped discovery, social platforms and global marketplaces.

• Discretionary demand is increasingly polarised, with confidence – not just income – determining where spending flows.

• Competition is shifting upstream as AI reduces search effort and shortens the path from intent to purchase.

• Investment priorities are shifting toward automation, capability building and operational resilience rather than pure expansion.

• Sustainability and circular behaviours are gaining traction, primarily driven by value rather than ethics alone.

• Success in 2026 will favour businesses that defend margins without eroding experience, embrace AI while elevating human touchpoints, and invest with clarity in a structurally changed market.

Introduction

As UK retail, hospitality and leisure businesses enter 2026, the turbulence of recent years has eased – but the conditions created have become structural.

The economy continues to expand, but at a modest pace. Inflation has moderated, yet remains sticky in core areas. Margins across consumer-facing sectors remain under sustained pressure.

This report sets out the macroeconomic backdrop, examines the evolving consumer landscape, and outlines how businesses can convert disruption into growth. The outlook for 2026 rewards businesses that defend margins without eroding experience, embrace AI while elevating human touchpoints, and invest with clarity in a market where confidence – not just income – determines spend.

Section 1: Operating backdrop – the margin squeeze

UK businesses enter 2026 against a backdrop of modest growth, easing but still-elevated inflation and a labour market that is softening but remains relatively tight.

Positively, the economy continues to expand, but at a slow pace, while margins in consumer-facing sectors remain under pressure. Together, these factors create a range of core expectations and impacts.

Across official forecasters, there is broad consensus that economic growth will be mildly positive in 2026, with real GDP projected between 1% and 1.5%. This reflects geo-political uncertainty, continued drag from fiscal consolidation, polarised consumer spending, and mixed productivity.

Despite challenging conditions, many consumer brands have continued to defy expectations. Those investing in digital capabilities, sharpening propositions around customer realities and leading with data-driven decision-making have consistently outperformed the market. This has been evident in a series of impressive Christmas trading updates, underlining how the strongest propositions are pulling ahead, even as performance remains uneven.

Autumn Budget impact –cost pressure without confidence

The Autumn Budget 2025 arrived at a sensitive moment for retail, hospitality and leisure. While further cost pressures were unwelcome, many businesses took reassurance from the fact that outcomes were less severe than feared, with greater clarity helping to support confidence.

Overall, six in ten businesses report feeling less confident after the Budget, citing business rates, tax headwinds and the cumulative burden of regulation as major causes of concern. However, there are signs the Government has responded to pressure from industry. A revised support package –worth around £100m annually –has been announced for pubs after warnings of widespread closures and job losses linked to the earlier business rates changes. This suggests the sector’s concerns have been heard, even if uncertainty remains.

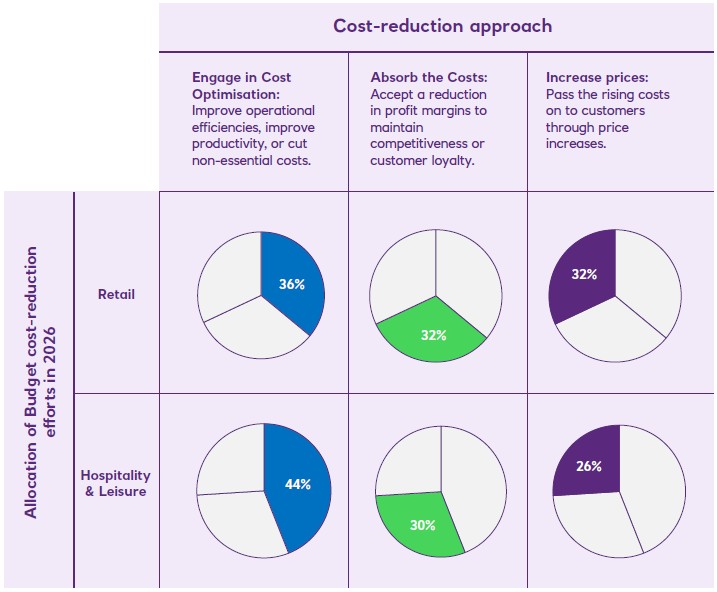

Fig [2] – How businesses are defending margins: cut, absorb or pass on?

Source: Retail Economics, Natwest

Risks and the cost mitigation

Businesses continue to rank cost-related risks as the most significant threat in 2026, scoring them high on both likelihood and severity of impact (Fig. 3). Pressures linked to trade, supply and input costs continue to weigh heavily on planning assumptions. Reassuringly, consumer and macro demand risks have eased, pointing to greater certainty and adjustment towards more stable demand levels.

-

Ongoing exposure to global supply chain disruption, higher import costs from tariffs and sanctions, energy price volatility, and less favourable foreign exchange continue to impact planning assumptions. While these risks are not new, they remain unresolved, keeping cost bases elevated and volatile.

-

Retailersare most concerned about business rates and taxation changes, reflecting the fixed-cost burden of large physical estates and uncertainty around future rate revaluations.

-

Hospitality, leisure and entertainment businesses highlight energy, insurance and input cost inflation as acute pressures, given exposure to utilities, insurance market hardening and venue-based operating models. Business rates revaluations remain a key concern, but transitional relief and the proposed £100 million support package are expected to soften the impact

Fig [3] – Cost, regulation and security dominate the 2026 risk landscape

Source: Retail Economics, Natwest

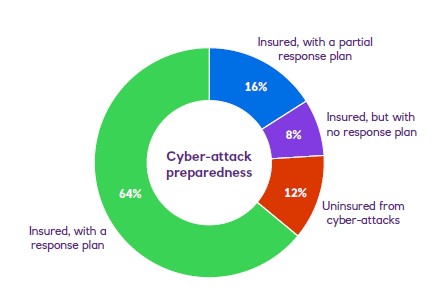

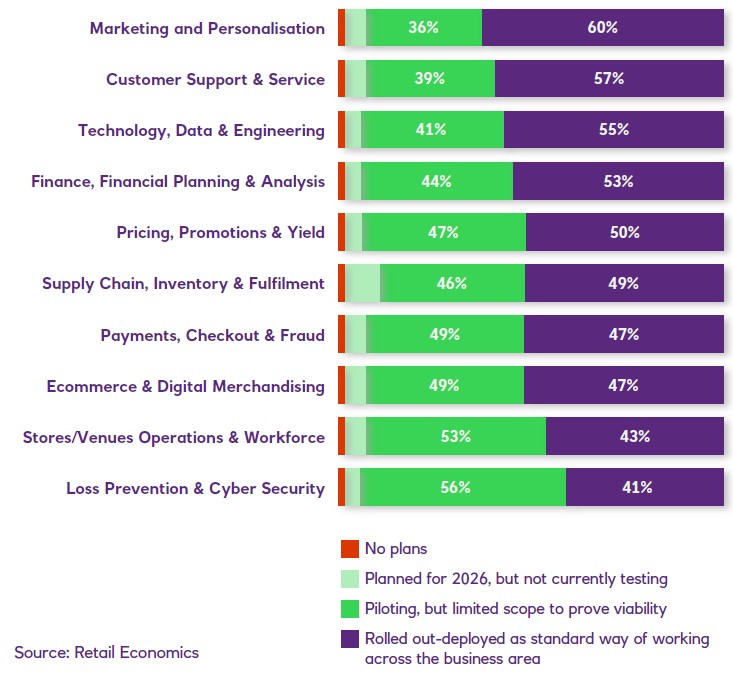

Cyber security

Cyber security has also moved rapidly up the risk agenda following continued high-profile attacks. As businesses deepen digital transformation – through AI integration, payments innovation and omnichannel fulfilment – cyber resilience has become a cornerstone of operational strategy.

In response, 56% of businesses plan to deploy AI within cyber security and loss prevention in 2026. This reflects the need to detect threats faster, reduce fraud and manage risk at scale amid a rise in perceived threats. Reassuringly, almost two-thirds of businesses (64%) have cyber insurance with a fully developed incident response plan (Fig. 4).

Fig [4] – Over a third of businesses are under-prepared for cyber-attacks

Source: Retail Economics, Natwest

Section 2: A more dynamic consumer landscape

Although overall spending volumes across retail, hospitality and leisure are forecast to rise modestly by 0.4% in 2026, performance remains highly uneven.

Discretionary volumes continue to underperform, while essential categories absorb a larger share of household budgets. Food and drink remains the most resilient category across cohorts – but for different reasons. Among lower-income households, it reflects necessity. Among affluent groups, it reflects premiumisation and trading up. Restaurants, hotels and leisure continue to see strong engagement from financially resilient consumers, who are driving higher spend per occasion despite overall volume pressure.

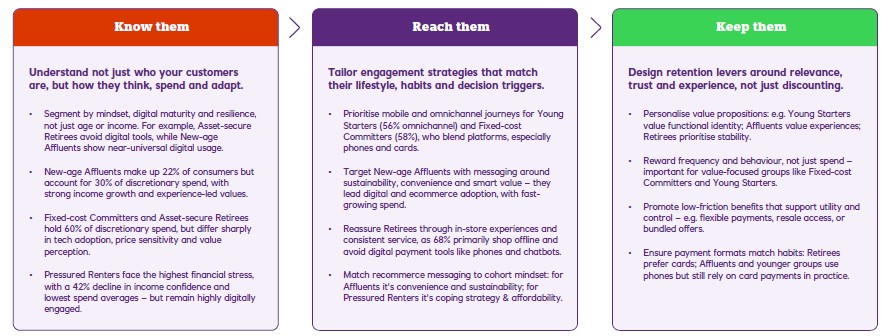

How to know, reach and keep your customers

In a fragmented market, customer retention relies on deeply knowing your customer, not just transactional data. Our three-step playbook outlines ways to help brands build deeper relationships and unlock targeted growth.

Fig [7] – Activating growth through deeper customer understanding

Source: Retail Economics, Natwest

The cost-of-living crisis is showing signs of improvement

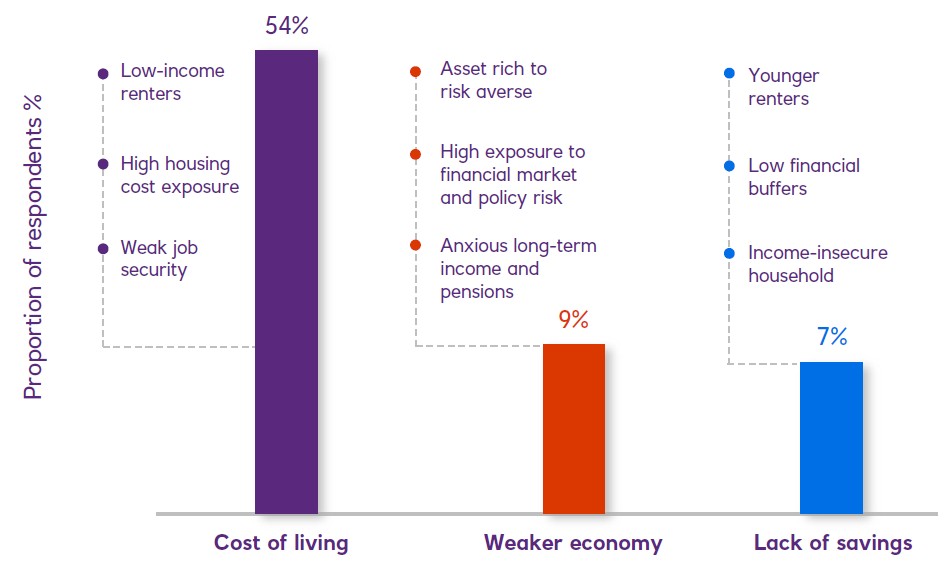

Despite modest improvements in household finances between 2025 and 2026, financial strain remains embedded across much of the consumer base. Incremental income gains are helping to stabilise household finances, though changes in core spending behaviour are likely to be gradual, reflecting an uneven recovery across consumer groups (Fig 9).

Interestingly, younger consumers are more willing to increase spending in 2026 despite ongoing pressure. This reflects greater optimism, while confidence among older and more exposed households remains subdued. Rising living costs continue to weigh on sentiment and are the leading concern for personal finances in 2026.

Essential spending continues to dominate lower-income budgets. Pressured Renters remain most constrained: 48.5% of income goes on food, drink and housing in 2026 (marginally below 2025), leaving minimal discretionary spend and driving weaker non-essentials. This compares to just 25.8% for New-age Affluents.

Fig [9] – Concerns vary by cohort as living costs dominate overall

Source: Retail Economics, Natwest

Saving continues to outpace spending in 2026, with households using savings as a security strategy amid uncertainty. However, buffers vary sharply between cohorts, reinforcing uneven resilience.

As perceptions of income certainty shift, discretionary demand becomes increasingly polarised. Large cohorts prioritise caution, while a smaller but influential group continues to spend through volatility. In 2026, confidence – not just income – is increasingly determining where spending flows.

Section 3: Five forces reshaping spend

AI commerce: AI is increasingly acting as a gateway to spend.

By reducing search effort and cutting through choice overload, AI shortens the path from intent to purchase for consumers. As a result, competition shifts upstream: businesses must optimise for discoverability across AI bots, marketplaces and social platforms – or risk losing visibility before the customer reaches their channels.

Fig [10] – AI is moving from test to standard across the value chain

Alongside AI, circular behaviours are gaining mainstream traction. As households look to stretch budgets and reduce waste, more are turning to repair, resale and buying pre-owned. While sustainability may not always be the primary driver, value-led circular models are becoming embedded in everyday purchasing decisions.

---