Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Homewares sales

Homewares sales rose by xx% year-on-year in May, matching the rate of growth recorded a year earlier. The category returned to more stable territory after April's decline, although the pace of growth remained well below that seen across clothing, health and beauty and electricals.

That outcome captures the mixed nature of consumer spending during the month. Households were more willing to spend than they had been earlier in the spring, helped by warmer weather, two bank holidays and improving confidence.

Much of that spending flowed into categories linked to summer living and seasonal occasions. Homewares benefited from some of those same trends, but demand remained concentrated in selected areas.

Key trading themes and drivers

The joint third warmest May on record provided a natural boost for parts of the category. Consumers spent more time at home and outdoors, supporting demand for seasonal home accessories, dining products, outdoor entertaining ranges and lighter furnishings.

Households showed a willingness to make smaller home purchases that delivered an immediate improvement to living spaces without requiring a significant financial commitment. Decorative accessories, soft furnishings and seasonal updates generally performed more strongly than larger discretionary purchases.

Retailer commentary points towards a similar pattern. Dunelm has continued to outperform much of the wider home market through its focus on value, convenience and broad product choice.

Digital channels continued to support growth. Homewares shopping often begins with inspiration, research and comparison, making online platforms an important part of the customer journey.

There was also an element of catch-up demand after April's weaker trading period. The combination of warmer weather and improved consumer sentiment encouraged households to revisit projects and purchases that had been postponed earlier in the spring.

That helped stabilise the category, but it did not translate into the stronger growth seen elsewhere across retail, with strong growth reported in clothing and electricals.

May felt like a month where consumers reengaged with the home, prioritising affordable refreshment over significant investment.

Macroeconomic backdrop

The consumer environment improved during the month, providing a more supportive backdrop for home related spending.

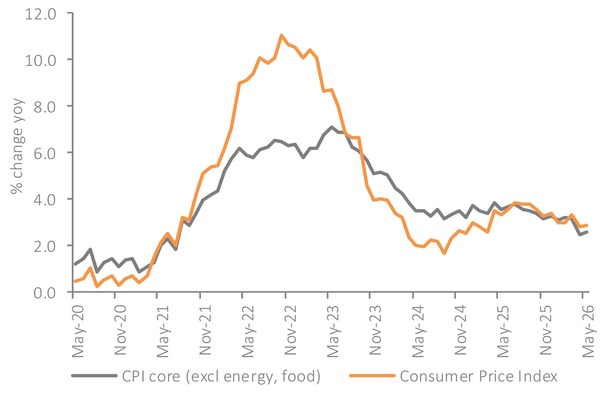

Inflation held at xx% for a second consecutive month, grocery inflation eased to a 17-month low and oil prices moved lower from the highs seen earlier in the year. Those developments reduced pressure on everyday household budgets and contributed to an improvement in consumer confidence.

Confidence improved for the first time in four months, but households continued to express caution around larger purchases.

The latest GfK data showed major purchase intentions falling to their lowest level since January 2025.

Homewares sits somewhere between everyday spending and major household investment, allowing it to perform better than furniture while still feeling the effects of consumer caution.

Interest rates remained unchanged at 3.75%, with expectations for rate cuts pushed further into the future.

Borrowing costs therefore remained elevated, limiting enthusiasm for larger home projects and renovations. Consumers continued to favour lower-cost updates and purchases that could be absorbed within existing household budgets.

The labour market also softened further during the month. Vacancy levels fell again; payroll employment remained below year-ago levels and wage growth eased. Households generally felt more comfortable than they had earlier in the year, but spending decisions remained disciplined

Take out a FREE 30 day membership trial to read the full report.

The Consumer Price Index rose by 2.8% in May year-on-year, unchanged from the previous month.

Source: Retail Economics, ONS

Source: Retail Economics, ONS