Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Furniture & Flooring – Retail Economics Index

Furniture and flooring sales rose by xx% year-on-year in May, returning to growth after April's decline. The result marked an improvement in trading conditions, although it fell short of the xx% increase recorded a year earlier and lagged the wider retail market.

May delivered one of the strongest retail months of the year, helped by two bank holidays, record-breaking sunshine and improving consumer confidence. Clothing sales surged, health and beauty maintained its momentum and electricals enjoyed a strong recovery. Furniture participated in the improvement, but only to a limited degree.

That gap says a great deal about the current consumer mindset, with households becoming more willing to spend during May, but much of that spending flowed towards categories that felt seasonal, immediate or relatively affordable.

Key trading themes and drivers

May felt more like a month in which the sector regained its footing after a difficult April.

Consumers spent more time outdoors, travelled during the bank holidays and directed spending towards summer-related purchases, although the uplift was not broad enough to generate a significant acceleration across the wider furniture market. Many households chose to refresh parts of the home while larger furnishing projects were kept on hold.

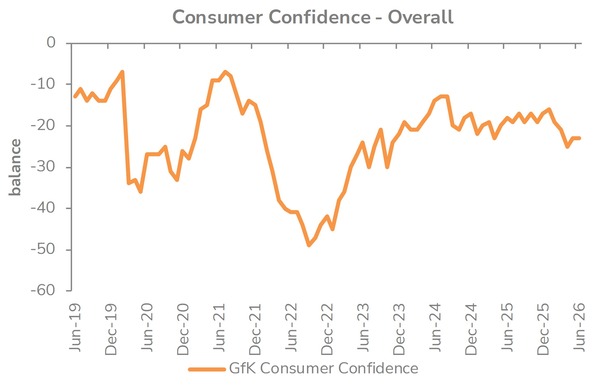

The category also continued to feel the effects of cautious decision-making. Consumer confidence improved during the month, but households remained hesitant when faced with larger commitments. The latest confidence data showed a growing divergence between attitudes towards everyday spending and major purchases.

Demand has been strongest where purchases solve immediate household needs or offer a visible improvement to daily living. The environment has been less supportive for big ticket discretionary purchases, where consumers continue to spend more time researching options and weighing up affordability.

Digital behaviour has become increasingly important in this process. Furniture shopping journeys are now heavily researched, with consumers comparing prices, reading reviews and evaluating delivery options before committing. Conversion is still achievable, but retailers are working harder to secure it than they were a year ago.

Housing activity offered some encouragement. Mortgage approvals reached their highest level since January 2025, and transaction levels have shown signs of stabilising. Furniture demand typically follows housing activity with a lag, meaning any benefit is more likely to emerge gradually during the second half of the year.

Macroeconomic backdrop

The economic environment became more supportive during May, helping to improve sentiment across the retail sector.

Inflation held at xx% for a second consecutive month and grocery inflation eased to a 17-month low. Falling oil prices also reduced concerns that another wave of cost pressures was about to emerge. After several months of uncertainty, households entered the summer feeling more comfortable about their short-term financial position.

Consumer confidence reflected that improvement, rising for the first time in four months. The detail beneath the headline, however, was particularly relevant for furniture retailers.

Views of personal finances improved, but the Major Purchase Index fell to its lowest level since January 2025. Consumers felt better about spending generally than they did about committing to expensive purchases.

Interest rates remained another constraint. The Bank of England kept Bank Rate at xx%, while financial markets pushed back expectations of rate cuts.

Mortgage rates edged higher during the month and borrowing costs remained elevated relative to recent years. Furniture purchases are often financed directly or indirectly through housing-related decisions, leaving the category especially sensitive to these conditions.

The labour market also softened further. Vacancy levels fell to their lowest point since early 2021, payroll employment remained below last year’s levels and wage growth eased again.

Employment conditions remain healthy by historical standards, but households are becoming more conscious of financial risk. When uncertainty rises, furniture purchases are often among the easiest expenses to postpone.

The backdrop was therefore better than it had been earlier in the spring, but not yet strong enough to unlock a return to big ticket spending.

Take out a FREE 30 day membership trial to read the full report.

Consumer confidence stable

Source: GFK

Source: GFK