Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

Retail Sales Performance:

May 2026 delivered a decisive upturn in UK retail sales, driven by exceptionally warm weather culminating in a record-breaking late month heatwave, two bank holiday weekends, as well as an easing in grocery inflation.

Growth increased xx% year-on-year according to the Retail Economics Retail Sales Index, up from April’s xx% fall.

Spending was strong in clothing and health & beauty, with big ticket purchases experiencing slower growth.

Factors impacting the headline performance in the month include:

Heat wave: While the first half of the month was cool and grey, a recording-breaking heatwave from 22nd-31st meant the Met Office confirmed May as the joint third warmest on record for the UK, and the hottest UK bank holiday Monday ever recorded on May 25. Demand rose sharply for summer clothing, sandals, outdoor toys, fans, lighter bedding, garden products and warm-weather homewares. The month completed the warmest spring on record for England and Wales.

Bank Holidays: The two bank holidays helped turn the warm weather into spend. Consumers had more time to shop, travel and socialise, with coastal towns and high streets seeing a visible lift late in the month. The timing supported fashion, grocery, leisure and selected home categories.

Cost pressures easing: Grocery inflation fell to a 17-month low and oil prices dropped from their March peak, giving households some breathing room.

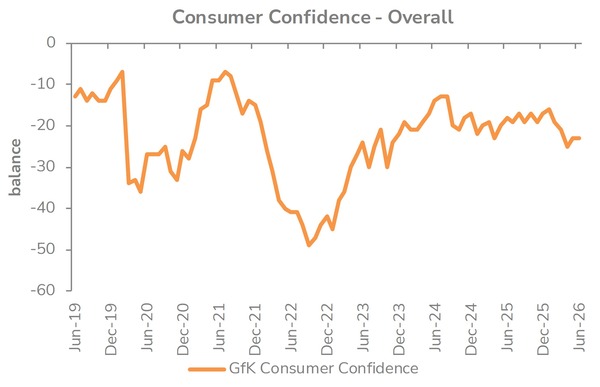

Underlying uncertainty: While spending improved, it was highly weather-sensitive, value-led, and concentrated around practical need or seasonal triggers. Caution did not disappear with GfK’s Major Purchase Index fell to its lowest level since January 2025 in May, showing continued hesitation around bigger commitments.

Macroeconomic backdrop

May’s domestic macroeconomic backdrop improved in parts but remained fragile.

Headline inflation held at 2.8% for a second month, down from a high of xx% in March. Grocery inflation fell, giving households some relief on everyday purchases.

Oil prices also eased as ceasefire diplomacy advanced in the Middle East. But the rise in the energy price cap in July is expected to push bills higher again, making Q3 a potentially more challenging period for discretionary spending.

Consumer confidence improved by two points to -xx. Personal finance views improved, but major purchase intentions fell to -xx, the weakest reading since January 2025.

The Bank of England held the bank rate at xx% at its June meeting, with seven members voting to hold rates and two members voting for a xx% rise to xx%. The Bank expects inflation to rise later this year as higher energy costs continue to feed through, and global energy prices continue to be volatile, remaining above pre-Iran conflict levels.

The UK labour market is cooling as firms respond to higher employment costs by slowing recruitment. Vacancies fell to their lowest level since early 2021, payroll employment was lower than a year ago, and private sector pay growth eased. Real regular pay growth remained close to flat, limiting the durability of any spending recovery.

Payrolled employees fell by xx (xx%) YoY in April. Compared with March, payroll numbers decreased by xx (xx%). Across February to April 2026, payrolled employees declined by xx (0.3%) year-on-year and by xx (xx%) on the quarter. Regular earnings growth stood at xx% YoY.

Housing offered mixed signals. Mortgage approvals reached their highest level since January 2025, giving some support to furniture, flooring, kitchens and appliances with a lag. House prices softened, mortgage rates edged higher and regional weakness persisted in southern markets.

Real GDP is estimated to have growth xx% in the three months to April, up from xx% in the three months to March. However, monthly GDP contracted by xx% in April.

Category impact

Food and grocery sales rose xx% in May. Food inflation eased slightly to xx%, its lowest level since December 2024. Promotional activity intensified as shoppers sought value.

Health and beauty (xx%) had another strong month, with demand for affordable indulgences, seasonal summer items, and low-priced necessities continuing.

Clothing and footwear had a strong month, with clothing sales growing xx% year-on-year, while footwear increased by xx%. The sector’s performance was driven by the warm weather, with consumers shopping for hot weather items and with demand concentrated in the final week of the month.

Electricals rose xx%, a strong improvement on the xx% rise recorded a year earlier. The category benefitted from early signs of demand for TVs and sound systems ahead of the World Cup.

Homewares grew xx%, supported by seasonal home purchases and online demand for summer-related ranges. Furniture and flooring rose xx%, an improvement from April, but still constrained by weak major purchase intentions and mixed housing indicators.

DIY and gardening rose xx%, helped by warmer weather and garden-related activity. Kingfisher’s update pointed to resilience in trade, e-commerce and marketplace growth. Larger projects remained more cautious, particularly where spend depends on housing confidence.

Take out a FREE 30 day membership trial to read the full report.

Confidence rose slightly in May

Source: Retail Economics, GFK

Source: Retail Economics, GFK