From blind spot to retail advantage: GNFR costs

DOWNLOAD FREE REPORT

10 minute read

How fashion retailers are turning GNFR into a margin lever

We surveyed 100 procurement, finance and operations leaders and analysed the 50 largest uk fashion retailers to quantify how GNFR is evolving

While leadership teams focus on merchandise margins and customer experience, a hidden cost structure is quietly eroding profitability across uk fashion retail. This report highlights how goods not for resale (GNFR) has become a material, fast-growing spend area, why it remains under-managed, and where retailers can unlock savings through better visibility, governance and procurement maturity. The prize is not just cost reduction – it is the ability to reinvest into innovation, resilience and operational performance at a time when growth remains muted.

What you can learn from this report

• How to identify the GNFR categories most likely to be driving hidden margin leakage in fashion retail operations

• Where GNFR governance typically breaks down across store and online models, and how to rebuild operational control

• How business maturity changes GNFR priorities, and what “good” looks like by retailer size band

• How to use a structured maturity framework to move from reactive procurement to strategic value creation

• Which operational capabilities to prioritise first so savings are repeatable, not one-off wins

Key report insights

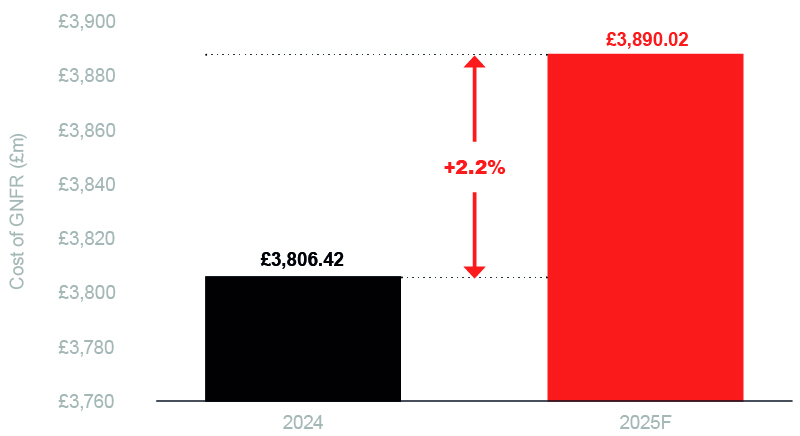

• GNFR across uk fashion retail is estimated to reach £3.9bn in 2025, representing a +2.2% increase on 2024 despite a weak sales backdrop.

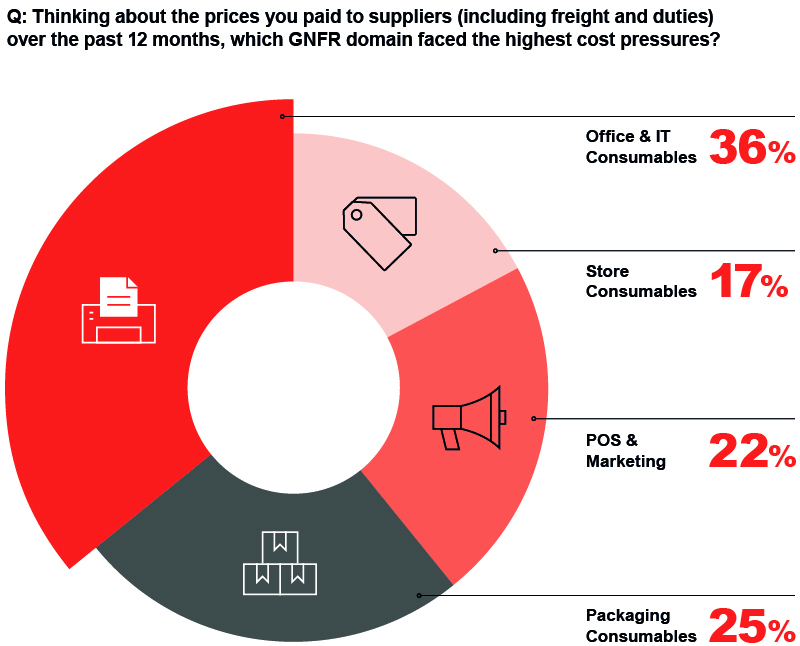

• Retailers report the sharpest GNFR cost pressures in everyday consumables, led by office and IT consumables (36%) and packaging and consumables (25%).

• Profitability is the most-cited GNFR priority for 2026, with 34% focused on maturity and capability development, 29% on sustainability and responsible sourcing, and 27% on resilience and process performance.

• Online models convert fulfilment and returns into variable GNFR costs, with online fashion return rates “around one in every four online clothing purchases”, valued at £8.2bn in 2025.

• GNFR is still viewed as a blind spot by many retailers, including 90% of medium-sized businesses and 87% of large businesses (agree/strongly agree).

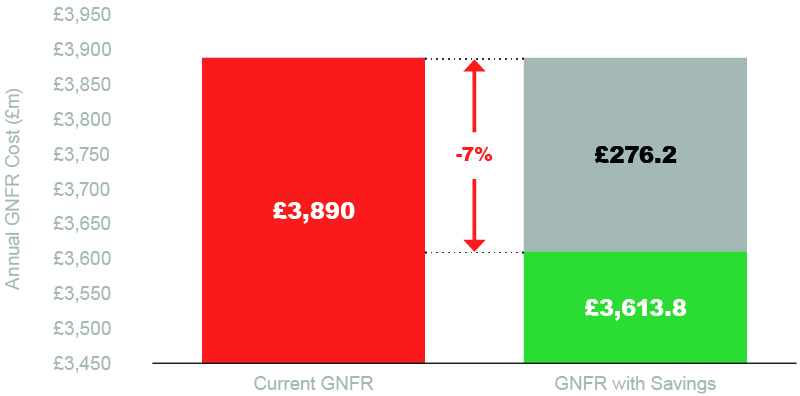

• A systematic 7% reduction in GNFR equates to £276.2m a year for uk fashion retail, equivalent to the profit on an extra £5.9bn of fashion sales (at a 4.7% margin).

• If retailers could free up 7% of GNFR spend, 35% would prioritise investment in innovation and transformation, ahead of improving operating margins (26%) or reinvesting in growth (25%).

Sneak peek at report insights...

Rising GNFR costs

GNFR represents one of the least visible cost areas in retail. It rarely features in earnings releases, yet it encompasses a wide set of essentials across packaging, consumables, facilities and more. To size the GNFR market for the UK clothing and footwear sector, we developed a topdown model using two key data inputs:

-

A business survey of 100 procurement, finance and operations leaders, capturing the proportion of turnover typically spent on GNFR.

-

The latest accounts of the 50 largest UK clothing and footwear retailers, validating turnover anchors and Opex structures. We found that GNFR across UK fashion retail is estimated to reach £3.9bn in 2025. This represents a 2.2% increase on 2024, despite the weak sales backdrop.

The increase aligns with three core structural trends:

-

Packaging inflation remains embedded following several years of supply disruption.

-

Wage costs have risen sharply and are being embedded into GNFR contracts.

-

Fashion retailers continue to manage elevated returns rates.

This increases the requirement for consumables, transit packaging and processing materials.

Figure 2 – The hidden cost of retail: GNFR rises to £3.9bn in UK fashion retail

Source: Retail Economics, CCS McLAYS

Pressure building in day-to-day operations

In our survey, respondents were asked which GNFR domains have seen the highest cost pressures in the past 12 months. The strongest responses were in the categories closely tied to day-to-day trading operations and store activity (Fig. 3).

-

Office and IT consumables (36%) were cited by more than a third of retailers. This reflects ongoing inflation in peripherals and essential equipment to support returns to offices amid hybrid working.

-

Packaging and consumables (25%) were next, influenced by ongoing adjustments to global freight markets, higher raw material costs and sustainability legislation.

These categories are essential for operations and are non-discretionary. They represent inescapable costs that retailers must absorb, manage, or mitigate through greater efficiency.

Figure 3 – Retailers report sharpest cost pressures in everyday consumables

Source: Retail Economics, CCS McLAYS

Physical vs. Online operations when it comes to GNFR

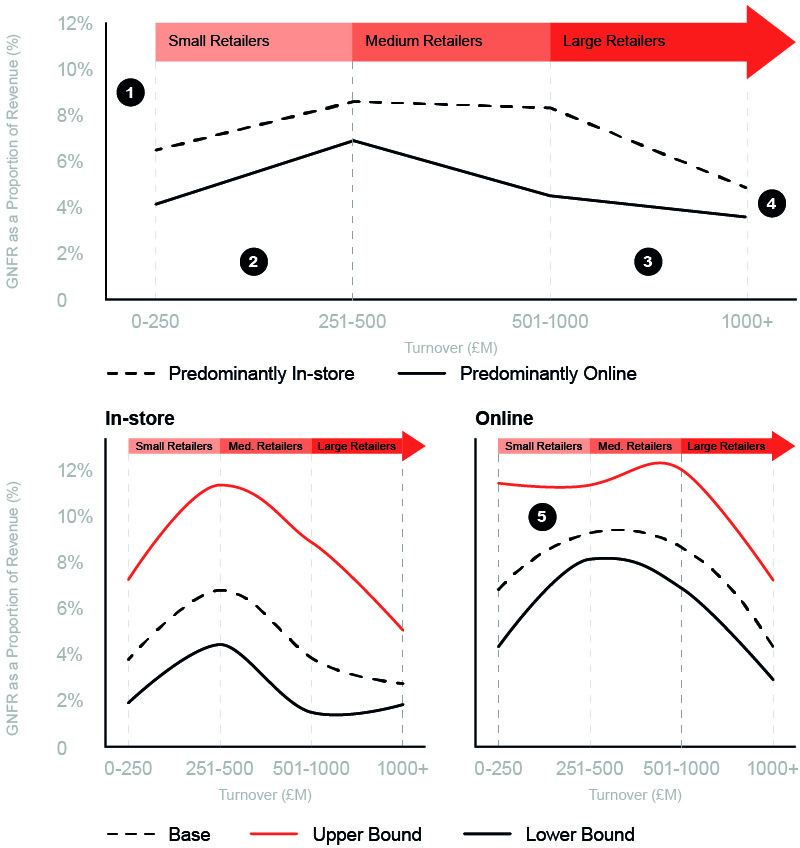

We compared GNFR costs as a proportion of revenue across four retailer turnover bands. The results show a clear and consistent pattern: across every size category, predominantly online retailers report GNFR costs around 2–3 percentage points higher than their store-based peers. These ratios matter because they highlight the differing GNFR intensity of retail business models.

Fixed store infrastructure dampens GNFR visibility

In store-based retail, large fixed costs such as rent, rates and staffing dominate the cost base. While GNFR costs may also rise with sales volumes, they represent a relatively smaller share of overall turnover and therefore play a less prominent role in the cost structure

Online models convert fulfilment and returns into variable GNFR costs

Predominantly online retailers operate with a fundamentally different cost profile. They avoid many fixed costs associated with a physical estate, such as rents, store fit-outs and shopfloor staffing, but instead incur higher variable GNFR costs.

Logistics, delivery and returns processing are particularly significant. Online fashion retailers face the highest return rates in the sector, with around one in every four online clothing purchases returned, valued at £8.2bn in 2025. Every online order requires outer packaging, protection materials, labels and documentation. This leads to materially higher consumption of boxes, mailers, tape, labels and paperwork per pound of revenue online. Each return generates incremental GNFR costs to inspect, repackage and reprocess items for resale or recycling.

These costs scale with... [download the full report to continue reading]

Figure 5 – The maturity curve of hidden costs across in-store and online models

Source: Retail Economics, CCS McLAYS

Significant GNFR savings potential

The maturity gap across the sector creates a significant opportunity for improvement. When asked what savings could be achieved through a systematic GNFR review, retailers estimated an average of 7%. Applied across the market, this equates to £276m a year for UK clothing and footwear. This value flows directly to operating profit. It does not require new stores, new channels or additional labour. It is operational headroom unlocked through better visibility, firmer governance and more consistent procurement practice.

To ilustrate the scale:

• A 7% GNFR reduction equals an 8.3% rise in sector operating profit.

• It matches the profit generated by £5.9bn of additional fashion sales at a 4.7% margin.

• £5.9bn in sales is equivalent to 983 million plain white T-shirts or 84 million mid-range trainers.

These figures may be conservative, as many businesses underestimate potential savings. CCS McLays often delivers savings of up to 20%, which would equate to £778m across the sector. This implies that a structured GNFR review is one of the most accessible levers for margin recovery in a low-growth market.

Figure 8 – A 7% saving in GNFR costs is equivalent to the profit on an extra £5.9bn of fashion sales

Source: Retail Economics, CCS McLAYS