Shades of Z: Decoding the next generation of consumers

DOWNLOAD FREE REPORT

5 minute read

The shades of Gen Z imperative: why one-size-fits-all retail strategies are failing

We surveyed 1,500 UK Gen Z consumers to decode how spend, digital behaviour and sustainability expectations are evolving

Gen Z will define the next decade of retail, but they are far from a single, predictable audience. Their behaviours can look contradictory: saving while splurging, digital-first yet store-reliant, and vocal on sustainability while remaining pragmatic in practice. This report challenges the stereotype-driven narrative by mapping four distinct cohorts and three behavioural themes, giving retail leaders a clearer route to win trust, relevance and lifetime value.

What we did

Retail Economics, in partnership with RSM, undertook consumer research in August 2025, surveying 1,500 UK Gen Z consumers aged 18–28. We used the findings to identify four distinct cohorts that bring Gen Z’s diversity into focus, and structured the analysis around three themes: shades of spend, shades of digital, and shades of green. Economic modelling and industry forecasts are based on proprietary Retail Economics data.

What you can learn from this report

• How to segment Gen Z beyond stereotypes using four distinct cohorts, and what each cohort needs from value, experience and convenience

• How Gen Z’s spend priorities are shifting by life stage, and how to align pricing, loyalty and proposition design to match their intent

• How discovery is changing from search-led journeys to social and mobile-first pathways, and what this means for conversion and attribution

• How to design seamless online-offline journeys that remove friction across browsing, buying, fulfilment and returns

• How to build credible sustainability and circular strategies that work in practice, not just in brand messaging

• What capabilities retail leaders should prioritise now, including personalisation, unified commerce foundations and social commerce execution

10 key insights

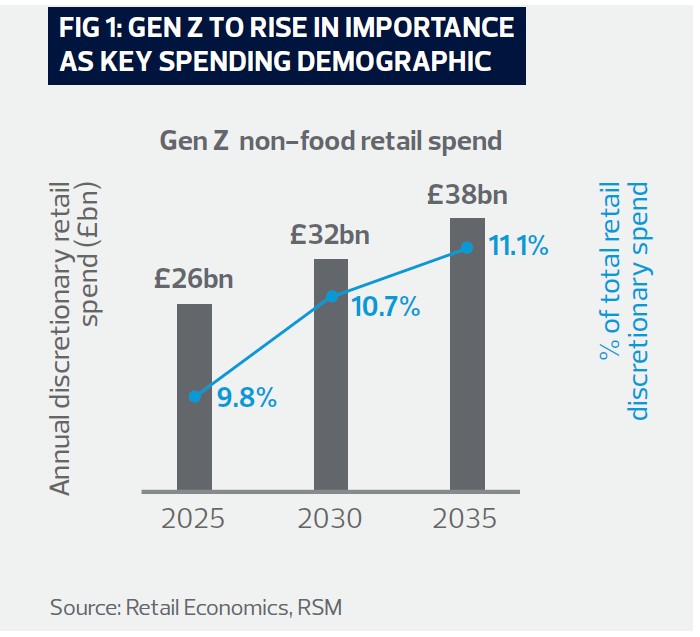

• Gen Z are set to drive over £26bn of retail spend in 2025, rising to almost £40bn by 2035, increasing their share of discretionary retail spend (Fig 1)

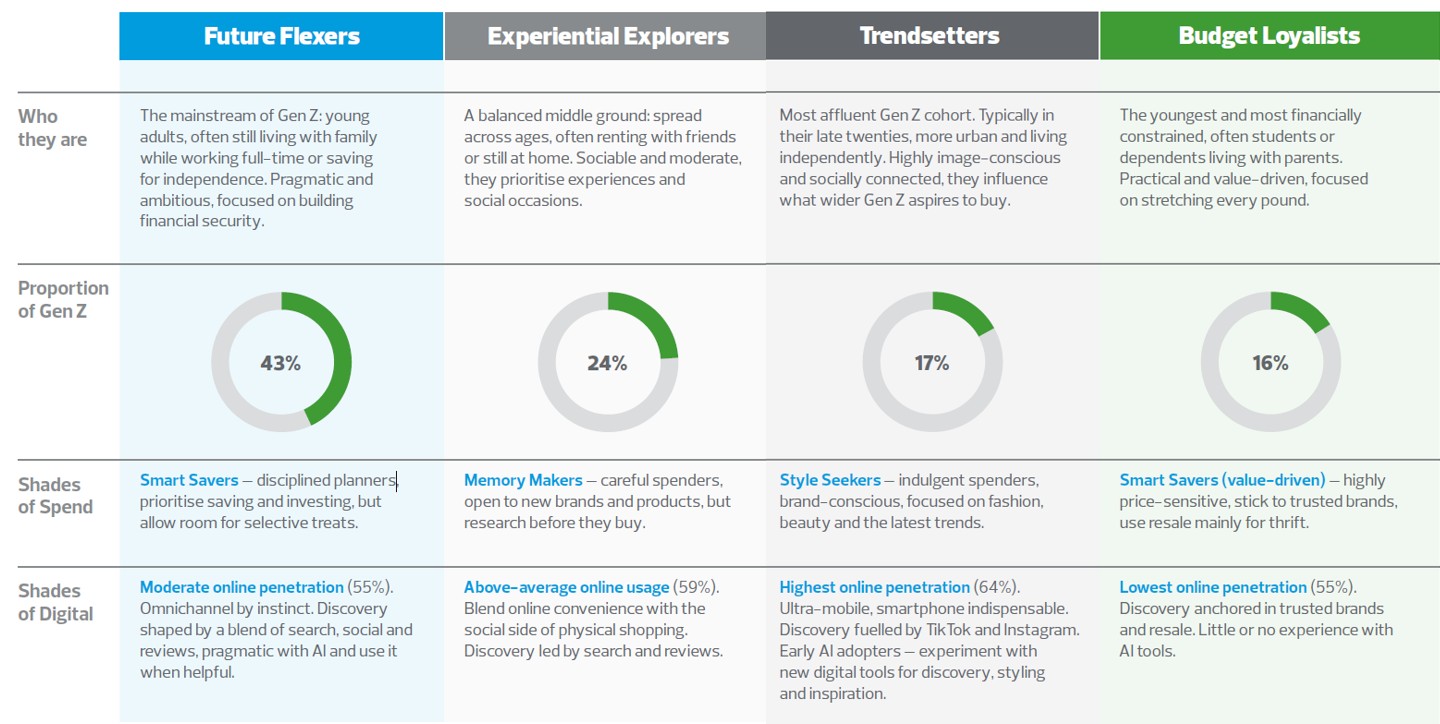

• Four cohorts sit beneath the Gen Z label, reinforcing why a single proposition, channel strategy or loyalty mechanic will underperform at scale (Fig 2)

• Gen Z are not reckless: when asked how they would use a £1,000 windfall, the biggest share would put it into savings or investments, signalling a strong planning mindset (Fig 4)

• Loyalty is conditional: only 28% consider themselves loyal to a small set of brands, underlining the need to continually re-earn relevance through experience, innovation and value

• Gen Z blend online and offline as standard, but are less likely than Millennials to shop purely online, with more identifying as store-first shoppers (Fig 6)

• Mobile is the gateway: 68% of Gen Z prefer shopping online via smartphone (vs. 51% of the typical UK consumer), shaping how discovery, conversion and loyalty must be designed (Fig 7)

• Social discovery is strongest for younger Gen Z: social overtakes search for 18–21s, changing the path from scrolling to store visits, purchase and post-purchase usage (Fig 8)

• The intent-action gap is real: 59% admit Gen Z talks more about sustainability than they practice, while 40% confess to buying items they will only wear or use once (Fig 9)

• Circularity is becoming mainstream behaviour: one in three (34%) Gen Z regularly shop pre-loved as an alternative to buying new (Fig 11)

• Ownership is increasingly fluid: almost half (47%) have re-sold an item within months of purchase, showing resale is now built into the purchase calculation for many consumers

Sneak peek at report insights...

Introduction

Gen Z is often treated as a single, unified group: digitally fluent, socially conscious and values-driven. But beneath the surface, this generation is diverse. Their behaviours, expectations and purchasing decisions vary depending on mindset, lifestyle and personal priorities.

Growing up through successive periods of rapid upheaval, Gen Z are the first mobile-first generation, raised on smartphones, social platforms and digital payments. Their formative years have been defined by a pandemic that rewired shopping overnight, a cost-of-living crisis that redefined value, climate anxiety that influences brand choices and now the rise of artificial intelligence (AI), all compressed into their teens and early twenties.

This volatility shows up directly in how they shop. They are the consumers behind #TikTokMadeMeBuyIt, driving viral impulse purchases, while simultaneously powering resale platforms such as Vinted. They expect always-on convenience through mobile commerce, Buy Now Pay Later and fast delivery as standard, yet still flock to stores for discovery, leisure and experience.

Inside Gen Z

A complex generation shaping the next decade of retail

Gen Z will define the next decade of retail. Born between 1997 and 2012, this almost 10 million-strong UK consumer group are approaching their prime spending years. Already reshaping shopping habits, their influence will accelerate as incomes rise.

They are set to drive over £26bn of retail spend in 2025, rising to almost £40bn by 2035. Yet Gen Z are not uniform. Too often, they are reduced to stereotypes: digital natives, socially conscious, values-driven. In reality, they are more fragmented, more demanding and harder to define than previous generations at the same life stage. Loyalties are weaker, expectations higher and preferences shift faster.

For retailers, there is no single playbook: within Gen Z itself, there are different shades to recognise and respond to.

Fig 1: GEN Z TO RISE IN IMPORTANCE AS KEY SPENDING DEMOGRAPHIC

Gen Z in focus

Our analysis of 1,500 UK Gen Z consumers revealed four distinct cohorts, each reflecting a different mindset and approach to shopping behaviours. They are not rigid boxes, but lenses that bring the diversity of this generation’s behaviours into focus.

Fig 2: Gen Z in focus: who they are, how they spend and what they value

Source: Retail Economics, RSM

Discover the 4 Gen Z consumer cohorts

📥 Complete the form to discover the 4 persona cohorts now - future-proof your export strategy