Report Summary

Period covered: May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Subscribe to access this data or take out a free 30-day subscription trial now.

Inflation

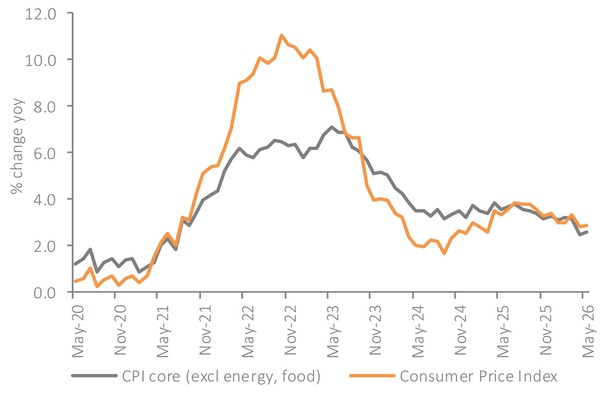

eadline inflation below expectations: CPI remained at xx% YoY in May, unchanged from April, with monthly inflation also the same rate as May last year. Economists had forecast a rise to xx%.

Core inflation edges higher: Core CPI rose to xx% YoY from xx% in April.

Goods inflation slowed to xx%, helped by weaker food and household goods inflation, while services inflation increased to xx% from xx%.

Transport inflation surges: Transport inflation accelerated to xx% YoY in May from xx% in April, reaching the highest rate since December 2022. Air fares, motor fuels and sea fares all pushed the category higher, along with the base effect from last year’s correction to Vehicle Excise Duty.

Food inflation eases again: Food and non-alcoholic drink inflation slowed to xx% YoY from xx% in April, the lowest rate since December 2024. Prices fell slightly on the month, compared with a xx% rise a year ago. Meat, dairy, vegetables and fish helped pull the rate lower, with only a small upward effect from oils and fats.

This lowers the pressure on the headline rate for now, but the relief may be short lived if fuel, fertiliser and energy costs feed through later in the year.

Furniture slips back into deflation: Furniture and household goods prices fell by xx% YoY in May, following a xx% rise in April. Prices still increased on the month, but by less than a year earlier, with furniture and furnishings driving the annual slowdown. Non-durable household goods provided some offset, led by higher prices for cleaning products.

Supply chain costs move against manufacturers: Producer price data points to a renewed squeeze on margins. Output price inflation eased slightly to xx% YoY but input cost inflation rose to xx% from xx%. That gap suggests that manufacturers are absorbing higher costs and not passing them on in full, increasing the risk of further price pressure later in the year if energy, transport and commodities remain elevated.

Markets have leaned towards an interest rate hold: Financial markets are pricing in just a xx% chance of an immediate interest rate rise, with policymakers widely expected to hold rates as they assess softer inflation, weaker food prices and the recent easing in oil markets.

Inflation outlook: May’s inflation data gives the Bank of England enough reason to hold policy steady for now, but the underlying data is more mixed. Services inflation has risen again, transport inflation is now at its highest rate since late 2022, and manufacturers are facing a wider gap between input costs and selling prices.

Inflation is still likely to rise in the summer, with July’s energy price cap increase adding pressure to household bills and fuel-related costs still feeding through parts of the basket. The peak in inflation could be lower than previously forecast if oil and gas prices remain close to current levels, but households are unlikely to feel much relief.

Softer food inflation helps preserve some spending power, but higher transport and energy linked costs will keep shoppers cautious. Pricing will become harder to manage for retailers if manufacturers pass on more of their cost increases later in the year.

Take out a free 30-day trial subscription to read the full report >

The headline Consumer Price Index (CPI) rose by 2.8% YoY in May, unchanged from the previous month

Source: ONS, Retail Economics analysis

Source: ONS, Retail Economics analysis