Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Health & Beauty - Retail Economics Sales Index

Health and beauty remained one of the strongest performers in May, with sales rising xx% YoY against a xx% increase recorded a year earlier.

Unlike other discretionary sectors that have experienced periods of volatility, health and beauty has delivered consistent growth throughout the past year with May extending that trend.

Consumers refreshed beauty routines, prepared for holidays and spent more time socialising outdoors amid the joint third warmest May on record, supporting demand across skincare, fragrance, cosmetics and personal care products. The result was another month in which health and beauty comfortably outpaced much of the wider retail market.

Key trading themes and drivers

The warm weather accelerated spending across sun care, skincare, grooming and beauty products as consumers adjusted routines for the summer months. Holiday preparation also started earlier than usual, bringing forward purchases that often build gradually through June.

Health and beauty continues to benefit from a different spending pattern to many other retail categories. Consumers may postpone replacing furniture, delay home improvement projects or cut back on larger discretionary purchases.

Personal care products, skincare routines and everyday beauty purchases tend to remain embedded within weekly and monthly spending habits.

Across the market, retailers have become increasingly effective at serving consumers who want to trade up and consumers who want to save money.

Social media also continues to influence demand. Product discovery is increasingly happening through TikTok, Instagram and creator driven content, helping retailers generate excitement around new launches and emerging trends. Beauty remains one of the few retail sectors where engagement often extends well beyond the point of purchase.

What has become more noticeable is the breadth of demand. Growth was not dependent on a single product area or a short-lived trend, with seasonal purchasing, wellness, premium beauty and everyday essentials all contributed to another strong month.

Macroeconomic backdrop

Economic conditions became more supportive during the month. Inflation remained at xx%, grocery inflation fell to its lowest level in more than a year and oil prices moved lower after the volatility seen in recent months.

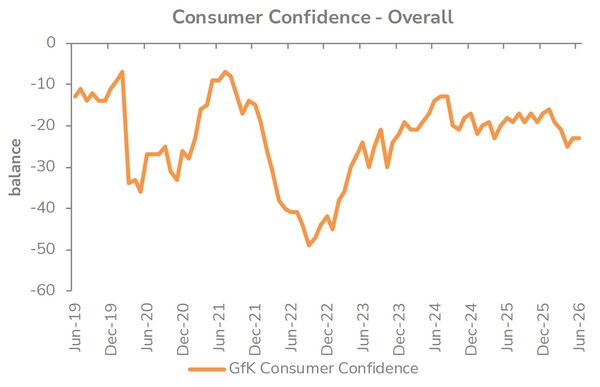

Consumer confidence improved for the first time in four months, with households feeling more positive about their personal finances and the wider economy. That improvement tends to feed quickly into health and beauty spending. Many purchases sit comfortably within everyday budgets, allowing consumers to increase spend without making major financial commitments.

The contrast between confidence and major purchase intentions was particularly remarkable. Consumers felt better about their financial position but remained reluctant to commit to expensive purchases.

Furniture, flooring and other big-ticket categories felt the effects of that hesitation, while health and beauty benefited from improving sentiment.

The labour market softened further during the month, with vacancy numbers continuing to decline and wage growth easing, encouraging greater discipline across household budgets.

Take out a FREE 30 day membership trial to read the full report.

Confidence edges up in June

Source: Retail Economics, GFK

Source: Retail Economics, GFK