Report Summary

Period covered: 03 May – 30 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

DIY & Gardening Sales

DIY and gardening sales rose by xx% year-on-year in May, accelerating from the xx% increase recorded a year earlier.

Long spells of sunshine and high temperatures moved consumers outdoors, bringing forward spending on gardens, barbecues, outdoor furniture and seasonal maintenance.

Two bank holidays created further occasions for households to spend time at home, host friends and make use of outside space.

Key trading themes and drivers

May is one of the most important trading months in the gardening calendar, and this year’s weather created the right conditions for seasonal purchases. Increased demand for garden furniture and barbecues supported performance, with the Spring Bank Holiday weekend providing a particularly strong boost.

Data from HTA showed transactions fell by xx% on last year, while average spend rose xx% as shoppers made fewer trips but spent more when they visited.

DIY spending drew support from warm weather which encouraged households to tackle outdoor repairs, painting, maintenance and smaller garden projects. Kingfisher has continued to benefit from strong digital sales and marketplace growth, while Wickes has reported steadier activity in repair, maintenance and selected installation projects.

May's growth came from people using their homes and gardens more, with large scale renovation spending remaining muted.

Macroeconomic backdrop

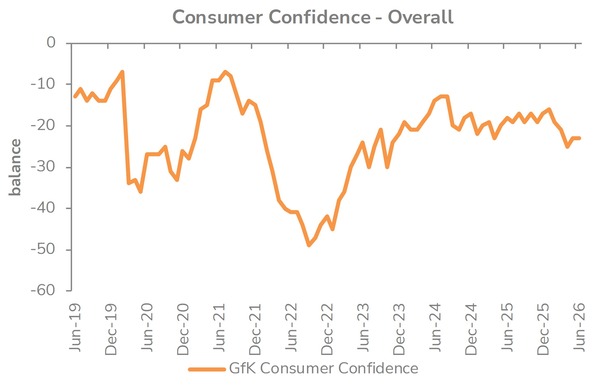

May brought some relief to household budgets. Inflation held at xx%, grocery inflation fell to a 17-month low and oil prices moved lower after the volatility earlier in the spring. Consumer confidence also improved for the first time in four months.

This supports categories where many purchases can be timed around the weather and made in stages. A household can spend £xx on seeds, or a tin of paint, then return later for the next part of a project.

However, the improvement had limits with GfK’s major purchases index falling to the weakest level since January 2025, and the Bank of England kept Bank Rate at xx%.

Mortgage rates edged higher, wage growth eased and the labour market continued to cool. These pressures are most visible in larger renovation work, landscaping and home improvement projects that require financing and professional installation.

Housing activity offered some support. Mortgage approvals reached their highest level since January 2025, and a steadier housing market should support repair and maintenance work.

Outlook

Summer weather will remain the main swing factor for DIY and gardening over the next few months. Continued sunshine would support outdoor furniture, barbecues and late-season gardening. A wet or unsettled period would quickly redirect spending towards maintenance and indoor projects.

Retailers will find demand for practical repairs and smaller projects easier to sustain than larger renovation work. Value, advice and convenience will remain important to consumers when researching and purchasing within the category.

The sector has entered summer with good momentum, but its fortunes will remain closely tied to weather patterns and the willingness of households to keep spending on their homes.

Take out a FREE 30 day membership trial to read the full report.

Consumer confidence stable

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK