UK DIY & Gardening Sector Report summary

October 2025

Period covered: Period covered: 31 August - 04 October 2025

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

DIY & Gardening Sales

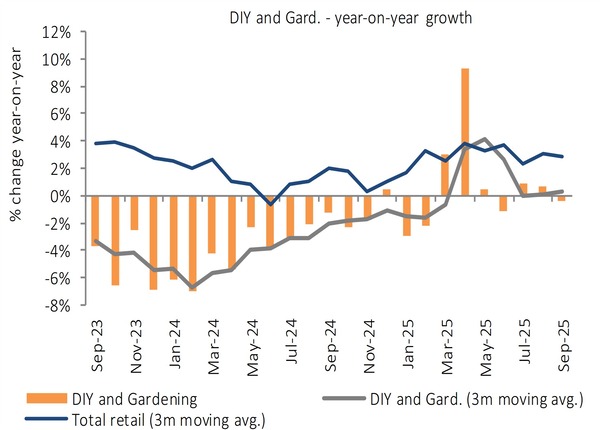

DIY and gardening sales declined by xx% year-on-year in September, marking the sector’s first negative result since June.

Although the drop was small, it reflected a broader slowdown in discretionary home improvement spend, with consumers continuing to prioritise essential outlay over more aspirational upgrades.

Key trading themes and drivers

Retailers saw demand fragment across categories. Core DIY categories were steadier than big-ticket renovation ranges, but customers increasingly focused on maintenance and repairs over transformational projects.

Promotions on consumables and seasonal lines helped to maintain footfall, but shoppers were selective in what they bought, often opting for more affordable alternatives or delaying non-essential purchases.

Garden centre boost

According to the Horticultural Trades Association (HTA), garden centres delivered small but consistent value growth in September. Sales rose by 3% year-on-year, with volumes up xx%, as customers remained engaged but traded down to more affordable products.

Gardening categories were flat overall, with live plant sales rising slightly, but hardy plants lagging levels seen two years ago. Bulbs and seeds were a bright spot, posting growth of xx% versus last year and up xx% on 2023.

Average transaction values were unchanged for the second consecutive year. Although steady footfall supported trade, margin pressures persisted, as customers gravitated toward smaller, lower-value purchases.

The HTA noted that while year-to-date sales are up xx% on 2024 and xx% on 2023, many operators still face challenges sustaining profitability due to rising operational costs.

Housing market activity

September brought a mixed picture for the housing market. Halifax reported that average UK house prices were xx% higher year-on-year, with the typical home now valued around £xx.

Mortgage rates hovered around xx%, still high by historical standards but down from earlier in the year. This has encouraged some households to stay put and invest in improvements rather than moving. That said, the scale of renovation activity remained limited.

Macroeconomic backdrop

The wider economic backdrop remained tight. Consumer confidence declined slightly in September, with GfK’s index falling to -xx. Inflation held at xx%, while pay growth of xx% ensured real earnings remained positive but weaker. However, rising unemployment (xx%) and declining job vacancies tempered overall household sentiment.

Credit conditions stayed restrictive, and many households continued to defer large purchases. For DIY and gardening, this meant trade was driven by affordability, necessity, and seasonal cues rather than ambition.

Take out a FREE 30 day membership trial to read the full report.

DIY & Gardening sales declined in September

Source: Retail Economics Retail Sales Index, value, non-seasonally adjusted

Source: Retail Economics Retail Sales Index, value, non-seasonally adjusted