UK Retail Sales Report summary

December 2025

Period covered: Period covered: 02 November - 29 November 2025

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

Retail Sales Performance

Retail sales growth rose xx% year-on-year in November according to the Retail Economics Retail Sales Index, compared to a three-month average of xx%.

Factors impacting the headline performance in the month include:

Mixed weather: Mixed weather impacted spending and demand for seasonal items, with an unseasonably mild start to the month delaying demand for winter clothing and footwear. A sharp temperature drop later in the month triggered catch-up buying, and heavy rainfall and Storm Claudia suppressed footfall on some days.

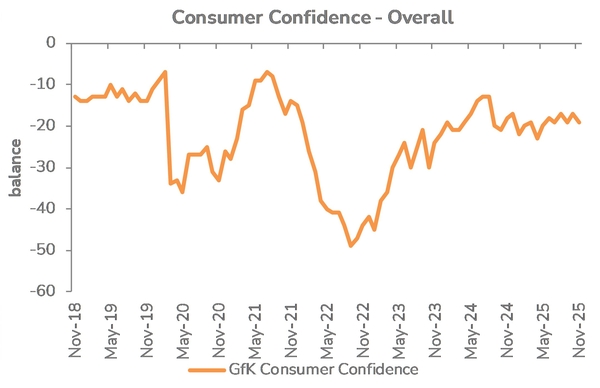

Cautious mood: Trading was influenced by fragile confidence ahead of the Budget late in the month. GfK confidence slipped back to xx, with major purchase intentions falling, emphasising a "wait and see" mindset at the start of peak trading.

Promotions-led spending: November sales were heavily skewed towards discount periods - Black Friday was included in the November trading period this year, having been in December a year ago.

Low footfall: Overall store visits trailed 2024 footfall. Black Friday delivered a short-lived uplift, with footfall up xx% week-on-week, but still xx% below last year's event. Retail parks outperformed high streets and shopping centres, reflecting more mission-led trips.

Category impact

This backdrop led retailers to offer deep discounts and promotions across the Black Friday period in a bid to encourage spend and overcome the uncertainty created by wider conditions.

Clothing sales rose by xx% YoY and Footwear rose by xx%, with demand shaped by the weather. A mild start to the month meant demand for seasonal items was low, resulting in retailers entering the promotional Black Friday period with excess winter stock.

Retailers offered significant discounts to entice shoppers, with clothing noted as a key factor in dragging November's inflation rate down. Despite the lowering of prices, YoY value growth increased over the month.

Health & Beauty sales grew by xx% YoY, with advent calendar and premium gift lines helping to boost sales throughout the month. Health-related sales also remained steady, and Black Friday helped unlock demand for prestige cosmetics and beauty technology.

Home categories performed well across the month, as consumers prepared their homes for Christmas hosting. Homewares (xx%) and Furniture & Flooring (xx%) benefitted from strong trade in products linked to hosting, such as household basics, and seasonal items such as lighting and decor also saw strong demand. Inflation in homewares has also been lower compared to other categories, meaning consumers are more willing to spend on smaller updates.

DIY and gardening (xx%) remained in positive territory in November, with seasonal purchases and small home upgrades also benefitting the category. Smaller home improvements to support festive gatherings also helped sales.

While sales data for electricals was strong (xx%), this was driven by deep discounts and large demand spikes over the Black Friday weekend. Outside of the promotional surge, however, underlying trade in electricals was challenging as consumers waited for deals, and margins were compressed as promotions drove sales.

Food sales rose xx%, with volume trends remaining mildly negative. Consumer spending remained needs-based and rooted in household necessity. Promotional activity accounted for xx% of all spend as retailers invested in price to drive footfall, according to Kantar. Grocery price inflation eased sharply to xx% as retailers intensified promotions. While many households continue to struggle, shoppers remained keen to treat themselves as Christmas approached.

Take out a FREE 30 day membership trial to read the full report.

Confidence falls back in November

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK