UK Retail Inflation Report summary

May 2026

Period covered: Period covered: 5 April – 2 May 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Subscribe to access this data or take out a free 30-day subscription trial now.

Inflation

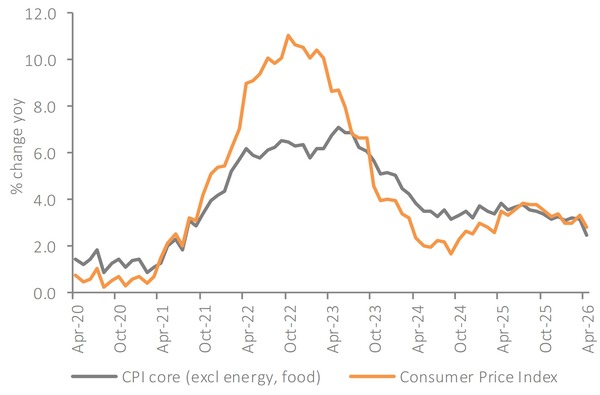

Headline inflation falls back: CPI eased to xx% YoY in April, down from xx% in March, with monthly price growth softer than a year ago. The drop was larger than many expected and gives households a short period of relief before energy and fuel pressures build again.

Core inflation cools sharply: Core CPI fell to xx% YoY, from xx% in March, helped by a notable easing in services inflation.

Services fell to xx%, down from xx%, while goods inflation moved higher, rising to xx%, driven partly by energy-linked categories.

Household bills pull inflation lower: Housing and household services made the largest downward contribution. Electricity prices fell sharply as the April energy price cap and government policy changes reduced household energy costs while gas prices also fell.

Fuel is now the main inflation driver: Motor fuel prices rose xx% YoY, the fastest annual increase since September 2022 due to the Middle East conflict. Petrol reached xxp per litre, the highest since November 2022, and diesel rose to xxp per litre, the highest since July 2022.

This was partially offset by air fares, which fell on the month after last year’s Easter timing pushed prices higher, pulling overall transport inflation down.

Food inflation eases: Food and non-alcoholic drink inflation slowed to xx% YoY, from xx% in March, with prices broadly unchanged on the month. Meat, confectionery, oils and fats, hot drinks and soft drinks all helped pull the annual rate lower.

Clothing returns to growth: Clothing and footwear inflation moved back into positive territory, rising xx% YoY after a xx% fall in March. The shift mainly came from garments and footwear, where last year’s discounting pattern was not repeated to the same degree.

Supply chain costs are rising again: There was renewed pressure on manufacturers with factory gate inflation rising xx% YoY in April while input cost inflation jumped to xx%. Higher energy, commodity, transport and packaging costs are squeezing margins, increasing the risk of price rises reaching consumers later in the year.

Inflation outlook: April’s fall in inflation gives the Bank of England some breathing room, but the improvement is unlikely to last.

Much of the decline came from regulated household bills and Easter timing. Fuel prices have already moved significantly higher, producer costs are rising again, and food supply chains remain exposed to energy and transport costs.

Inflation is likely to climb back through the second half of the year, with the risk moving from household bills to the everyday costs consumers notice most, including petrol, groceries and essentials.

Retailers are likely to face a more defensive spending backdrop, with value, promotions and price becoming more important as household budgets tighten again.

Take out a free 30-day trial subscription to read the full report >

The Consumer Price Index rose by 2.8% in April year-on-year, down from 3.3% in the previous month.

Source: ONS, Retail Economics analysis

Source: ONS, Retail Economics analysis