UK Retail Inflation Report summary

February 2026

Period covered: Period covered: January 2026

3 minute read

Inflation

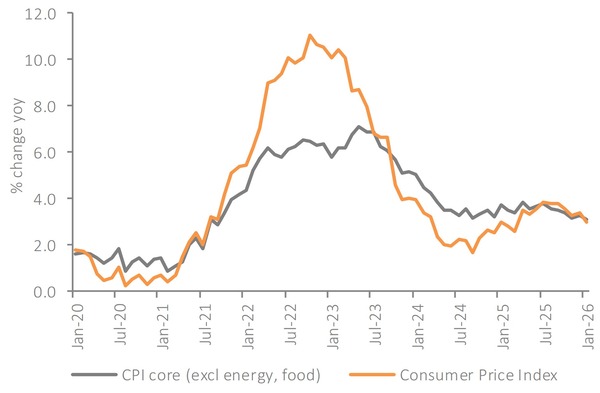

Headline inflation drops sharply: CPI fell to xx% in January from xx%, its lowest level since March 2025. Monthly prices declined xx% following December’s seasonal pressures.

Goods and service inflation ease: Goods inflation fell sharply to xx%, down from xx%, while services inflation also eased, albeit at a slower pace to xx% (from xx% in December).

Transport delivers the largest drag: Annual transport inflation fell to xx% from xx%. Fuel prices declined materially on the month, and air fares unwound December’s surge in a more typical seasonal pattern. Motor fuel inflation has now turned negative, removing a persistent source of pressure.

Food inflation cools sharply: Food and non-alcoholic beverages slowed to xx% from xx%, with prices falling slightly on the month. Six of eleven grocery categories contributed to the slowdown, including staples such as bread, meat and dairy. This marks the lowest food inflation reading since spring 2025.

Restaurants and hotels firm: Inflation in this category rose to xx%, up from xx%. Seasonal accommodation pricing patterns were less aggressive than a year earlier, lifting the annual comparison even as monthly prices fell.

Education distortion fades: Education inflation dropped to xx% from xx% as the impact of last year’s VAT change on private school fees fell out of the annual comparison.

Producer price pressures retreat: Factory input costs fell xx% year-on-year, reversing December’s increase. Output prices slowed to xx%. The combination of falling input costs and slower output price growth indicates that pipeline inflation has weakened materially, reducing the need for further price increases across consumer facing sectors.

Financial markets respond positively: Rate cut expectations strengthened, with markets assigning an xx% probability to a March reduction, up from xx% a week ago. Following the release of the inflation figures, the FTSE 100 reached a fresh high as investors anticipate an easing cycle gaining traction.

Inflation outlook: January confirms that the inflation pulse is weakening. Transport and food have shifted firmly into disinflation, and goods pricing is now subdued.

Food inflation has moved back in line with central bank projections and no longer presents a material upside risk. Price competition at supermarket level remains intense, and upstream cost measures have stabilised.

Services inflation remains the area of greatest persistence. Catering and other demand-sensitive categories continue to exhibit firm pricing. However, wage growth has cooled markedly and rental inflation is easing, which will weigh on services over coming months.

Inflation is set to move closer to target by the second quarter and could briefly dip below 2% before settling around that level through the summer, supporting a gradual easing path.

For households, fuel costs are lower, food inflation is cooling, and goods prices are no longer rising at pace. Stability is replacing volatility, creating firmer ground beneath consumer confidence as the year progresses.

Take out a free 30-day trial subscription to read the full report >

CPI fell to 3.0% in January from 3.4%, its lowest level since March 2025

Source: ONS, Retail Economics analysis

Source: ONS, Retail Economics analysis