UK Health & Beauty Sector Report summary

March 2026

Period covered: Period covered: 01 February - 28 February 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Health & Beauty - Retail Economics Sales Index

Health and beauty sales rose by xx% year-on-year in February, outperforming all other non-food categories and accelerating from the xx% increase recorded a year earlier.

The category continued to benefit from consistent demand and a degree of insulation from broader discretionary pressures.

Key trading themes and drivers

February extended the strong start to the year for health and beauty, with demand supported by a combination of seasonal factors and structural consumer priorities. The category continued to benefit from a focus on wellbeing, personal care and routine-driven purchasing behaviour.

Unlike other discretionary sectors, demand was not heavily dependent on promotional cycles. While targeted offers remained present, particularly online, sales were driven more by sustained purchasing patterns than by discount-led spikes. This supported both value and volume growth across core categories.

Consumer behaviour continued to favour smaller, frequent purchases. Given health and beauty products sit at a lower price point relative to other discretionary goods, households can maintain spending in the category even while tightening budgets elsewhere. This small treat dynamic, or “lipstick effect”, remained a key driver of resilience.

Seasonal demand provided an additional boost. Valentine’s Day supported sales of fragrance and cosmetics, while winter health needs sustained demand for over-the-counter medicines, vitamins and supplements. These factors combined to create an uplift across multiple segments within the category.

Digital channels played an important role, particularly in driving awareness and conversion through social media and targeted marketing. Online platforms supported product discovery and repeat purchasing, contributing to the category’s overall growth.

Macroeconomic backdrop

The macroeconomic environment remained challenging, with geopolitical developments adding a new layer of uncertainty during the month.

Household finances remain under pressure, with consumers prioritising essential spending and carefully managing budgets.

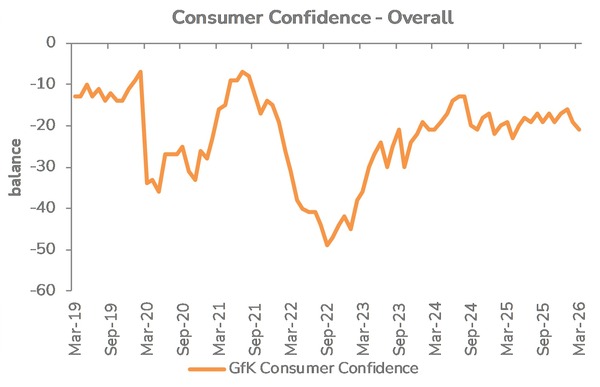

Consumer confidence weakened during February, reflecting increased concern around inflation and the broader economic outlook. Despite this, spending in health and beauty remained resilient, supported by its mix of essential and affordable discretionary products.

Inflation trends were broadly stable in February, with CPI holding at xx% year-on-year and rising xx% on the month. Food and non-alcoholic beverage inflation eased to xx% year-on-year, offering some relief in household budgets.

However, the outlook for inflation has become less certain following the escalation of conflict in the Middle East late in the month. Rising oil and energy prices have introduced upward pressure on the near-term path for inflation, with expectations now pointing to CPI remaining closer to xx over the coming quarters and could peak around xx later this year.

Monetary policy has responded with greater caution. Interest rates were held at xx, with expectations for near-term reductions pushed further out as policymakers assess the impact of higher energy costs. This prolongs pressure on household finances and supports a cautious approach to discretionary spending.

Outlook

The outlook for health and beauty remains positive relative to the wider retail market. The category is well positioned to continue outperforming, supported by consistent demand and strong consumer engagement.

Seasonal drivers and ongoing wellness trends are expected to sustain growth, with continued interest in skincare, health and personal care products.

While broader economic uncertainty may limit discretionary spending, the category’s lower price point and essential characteristics should continue to support demand.

Health and beauty is expected to remain one of the strongest performing retail categories in the near term, delivering growth even as wider market conditions remain challenging.

Take out a FREE 30 day membership trial to read the full report.

Confidence fell two points to -21 in March

Source: Retail Economics, GFK

Source: Retail Economics, GFK