UK Health & Beauty Sector Report summary

February 2026

Period covered: Period covered: 04 January - 31 January 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Health & Beauty - Retail Economics Sales Index

Health & beauty sales rose by xx% year-on-year in January, outperforming all other non-food categories and marking the strongest start to the year across discretionary retail. The category benefited from behavioural tailwinds associated with New Year routines.

Performance was notably ahead of broader non-food growth, highlighting the sector’s relative insulation from big-ticket hesitation and its alignment with everyday spending priorities.

Key trading themes and drivers

January’s performance was driven by a powerful combination of behavioural intent, accessible price points and strong digital engagement.

The New Year reset remains a defining feature of the category. Consumers prioritised wellbeing, fitness and personal care, driving demand for vitamins, supplements, skincare, personal grooming devices and health-focused food and drink. Demand reflected deliberate purchasing decisions aligned with lifestyle goals. Retailers reported sustained interest in high-protein nutrition and premium skincare routines as consumers sought structured self-improvement.

Gift card redemption also played a meaningful role. Christmas gift vouchers, frequently used in beauty retail, converted into January store and online traffic. This created incremental sales without requiring deep discounting, supporting margins relative to other discretionary sectors.

Digital influence was particularly pronounced. Social media platforms continued to influence product discovery, with viral beauty trends and wellness challenges translating into rapid online conversion.

Pricing discipline remained firmer than in other non-food categories. While selective promotions were present, the sector relied less on aggressive clearance and more on product innovation and brand loyalty.

Cold, wet weather increased time spent indoors, sustaining interest in skincare, haircare and self-care treatments that can be performed at home. Spending on digital content and streaming rose during the month, highlighting broader home-based lifestyles that complement health and beauty consumption.

January’s outperformance reflects structural resilience, behavioural alignment and effective digital execution rather and was more than a short-term promotional spike.

Footfall patterns

Total retail footfall declined year-on-year in January, yet health & beauty retailers demonstrated stronger conversion than many discretionary peers. High street locations experienced softer browsing traffic during adverse weather, but the category’s habitual purchasing nature mitigated volatility.

Outlook

Health & beauty enters 2026 with strong momentum and structural demand drivers that extend beyond seasonal promotion cycles. January’s performance demonstrates that consumers continue to prioritise wellbeing and personal care even within a restrained spending environment.

Growth is likely to slow from January’s elevated rate as resolution-driven purchasing tapers through February. However, recurring replenishment patterns, subscription models and continued digital engagement should sustain above-market performance.

As inflation continues to ease and confidence stabilises, the category is well positioned to maintain steady expansion. The principal risk lies in competitive intensity and promotional dependency as retailers seek to defend share.

Take out a FREE 30 day membership trial to read the full report.

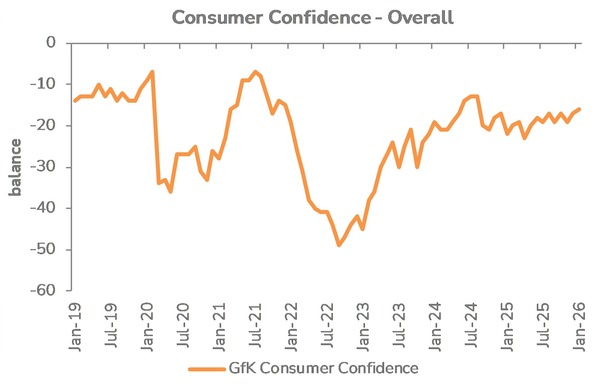

Confidence rose by one point to -16 in January

Source: Retail Economics, GFK

Source: Retail Economics, GFK