UK Furniture & Flooring Sector Report summary

December 2025

Period covered: Period covered: 02 November - 29 November 2025

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Furniture & Flooring - Retail Economics Index

Furniture and flooring sales rose by xx% year-on-year in November, a reversal from the xx% decline recorded in the same month last year.

Key trading themes and drivers

Promotion-led spending: November's growth was amplified by the inclusion of the Black Friday promotional period, which fell outside of the comparable period in 2024.

This calendar distortion elevated year-on-year comparisons and brought forward a significant volume of seasonal spending.

Deep discounts and extended promotional periods helped unlock latent demand. Sofas, beds, and dining sets were prominent in campaigns, supported by interest-free credit and flexible delivery windows.

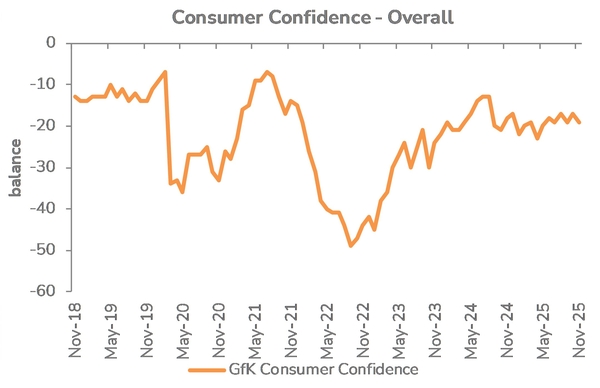

Cautious mood: Trading was influenced by fragile confidence ahead of the Budget late in the month. GfK confidence slipped back to -xx, with major purchase intentions falling, emphasising a "wait and see" mindset at the start of peak trading.

Footfall patterns

Footfall was inconsistent across the month, tracking below 2024 levels for much of November before recovering during the Black Friday week.

Retail parks performed better than high streets or shopping centres, in part due to the location of furniture and flooring retailers.

Nevertheless, store traffic remained uneven and online remained an important channel for research and sales conversion.

Macroeconomic backdrop

November's economic climate presented a mix of easing inflation and persistent caution.

Falling CPI inflation to xx% improved real income sentiment marginally, but confidence remained low ahead of the Autumn Budget.

The drop in inflation was driven in part by retail discounting, which extended to the home sector.

Wage growth slowed and unemployment ticked higher, yet interest rate expectations shifted positively, culminating in a December rate cut.

These factors contributed to a slightly more supportive environment for considered purchases, though the uptick in sales appears more linked to promotional timing than underlying demand strength.

Housing market

The housing market remained subdued but broadly stable in November. Nationwide reported slight monthly price rises, though annual growth slowed to xx%.

Buyer enquiries fell ahead of the Budget, and mortgage activity remained below average. That said, expectations of interest rate cuts supported sentiment modestly, with affordability pressures easing slightly.

For the furniture and flooring sector, the lack of a housing shock helped maintain a degree of home-related spend.

Many consumers opted to invest in their current properties rather than move, boosting replacement purchases and interior upgrades.

Outlook

Furniture and flooring retailers will now look to December to maintain momentum.

While Black Friday distorted November's comparison, the strength of seasonal categories and sustained interest in home environments provide some grounds for cautious optimism.

However, the reliance on promotions and the lingering effects of economic uncertainty mean further growth is likely to be uneven.

The sector remains one of the weaker parts of discretionary retail, with its performance hinging on both consumer confidence and the timing of discount-led activations.

Take out a FREE 30 day membership trial to read the full report.

Confidence slips as households brace ahead of budget

Source: GFK, Retail Economics analysis

Source: GFK, Retail Economics analysis