UK Furniture & Flooring Sector Report summary

April 2026

Period covered: Period covered: 01 March - 04 April 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Furniture & Flooring – Retail Economics Index

Furniture and flooring sales rose by xx% year-on-year in March, a marginal improvement on the previous month but still below the xx% increase recorded a year earlier. The headline suggests stability, yet it masks a clear loss of momentum as the month progressed.

Early trading conditions offered some support, but this faded quickly, leaving the category exposed to a more cautious consumer. Value growth remained weak, with volumes under pressure as households defer higher-cost purchases.

Key trading themes and drivers

Trading followed a familiar pattern seen across discretionary categories. The first half of the month benefited from seasonal factors, including improved weather and key retail events, which supported showroom visits and online browsing.

Momentum shifted sharply in the second half. The escalation of conflict in the Middle East weighed on sentiment, prompting households to delay major spending decisions. This behavioural shift is particularly acute in furniture and flooring where purchases are often planned and easily postponed.

The decline in big-ticket purchasing appetite, along with a rise in precautionary saving, points to a customer base that remains engaged but increasingly hesitant.

Demand has become more promotion-led, with customers trading down or waiting for clearer signs of value before committing. Delivery timing and order pipelines have also introduced volatility into monthly readings, further masking underlying softness.

Impact on retail categories

Furniture remained one of the weakest components within the broader category, with demand subdued as households postponed larger purchases. Sofas, beds and dining furniture were particularly affected, reflecting their high discretionary nature.

Online channels provided some resilience, particularly for browsing and price comparison, but conversion rates weakened later in the month as confidence deteriorated.

The category’s close link to housing transactions continues to act as a constraint. With fewer consumers moving home or committing to major upgrades, demand remains structurally subdued.

Macroeconomic backdrop

The macroeconomic backdrop became less supportive as March progressed. Inflation rose to 3.3% year-on-year, driven in part by higher fuel costs and upward pressure in services. Food inflation also moved higher, adding to household cost pressures.

The escalation of conflict in the Middle East has introduced a new source of uncertainty. Rising energy and commodity prices are expected to feed through into inflation over the coming months, increasing pressure on real incomes.

Monetary policy expectations have shifted accordingly. Interest rates were held at 3.75%, but expectations for rate cuts have been pushed out. Mortgage pricing has firmed, increasing the cost of borrowing for households and directly impacting affordability in the housing market.

Housing market indicators present a mixed picture but point towards softer conditions ahead. More telling is the shift in financing conditions, with higher swap rates feeding into mortgage pricing and weighing on buyer demand.

Mortgage approvals had shown some improvement earlier in the year, but the latest developments suggest this momentum may not be sustained. As borrowing costs rise and uncertainty increases, transaction volumes are likely to soften.

The labour market continues to ease, with wage growth slowing and employment indicators softening at the margin. While this reduces inflationary pressure, it limits the scope for real income growth to support discretionary spending.

For furniture and flooring, this is translating into a more cautious consumer, with higher financing costs and a softer housing market all pointing to continued pressure on demand.

Take out a FREE 30 day membership trial to read the full report.

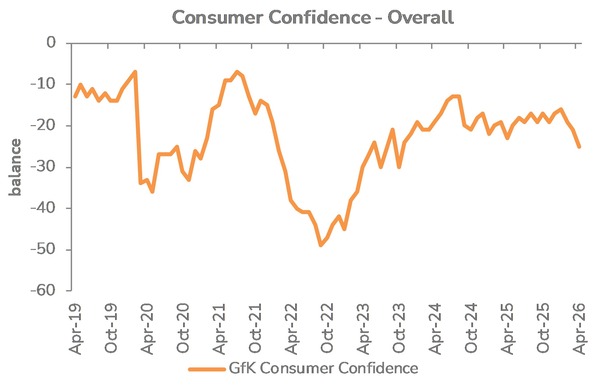

Confidence fell four points to -25 in April

Source: GFK

Source: GFK