UK Food & Grocery Sector Report summary

February 2026

Period covered: Period covered: 04 January - 31 January 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Food & Grocery Sales

Food and grocery sales rose by xx% year-on-year in January, ahead of the xx% increase recorded in the same month last year.

The result marginally outpaced official inflation, which eased to xx% in January, indicating broadly stable volumes following the festive period.

Key drivers and category performance

- January trading reflected a post-Christmas reset in shopper behaviour, with promotional participation increasing sharply. Sales on promotion rose by xx% year-on-year, compared with growth of just xx% in full-price sales. Retailers intensified price visibility across staple lines including fresh produce, dairy and proteins to defend volumes and highlight value perception.

- Own-brand products accounted for a record xx% of total grocery spend in January, as households substituted branded alternatives in favour of lower-priced equivalents. Entry tier and core own-label ranges performed strongly, while premium own-label retained engagement in health aligned and meal planning categories.

- Nearly a quarter of households reported actively seeking high-protein or high-fibre foods during the month, supporting growth in fresh fruit and vegetables, poultry and dairy lines. Low- and no-alcohol sales rose by around xx% year-on-year during Dry January, partially offsetting softer traditional alcohol volumes.

- Online grocery maintained positive momentum amid adverse weather conditions.

- Storm disruption and persistent rainfall encouraged greater use of delivery and click-and-collect services, with online food sales growth rising by xx% YoY, it’s strongest rise since September 2023.

- Competitive intensity remained elevated. Discounters continued to post above-market growth, while established supermarkets relied on loyalty pricing and personalised offers to retain spend.

Macroeconomic backdrop

The macroeconomic backdrop became incrementally more supportive at the start of 2026. Headline inflation eased to xx%, reducing pressure on disposable income. Food inflation, while still elevated, continued its downward path, limiting the risk of renewed strain on household budgets.

Wage growth remained ahead of inflation, sustaining real income growth. Consumer confidence improved to xx, driven largely by improved sentiment around personal finances.

Interest rates were held at xx%, with market expectations building for gradual reductions as early as Q1 2026.

Recent data from the Bank of England indicate that consumer credit growth remains elevated, with credit card borrowing expanding at double-digit rates year-on-year. This suggests that some households continue to lean on unsecured credit to smooth expenditure, including grocery spending during higher-cost periods.

The housing market showed early signs of improvement, with house prices rising month-on-month and returning to annual growth in January. A steadier property market supports broader financial stability, indirectly supporting consumer confidence in day-to-day spending.

Take out a FREE 30 day membership trial to read the full report.

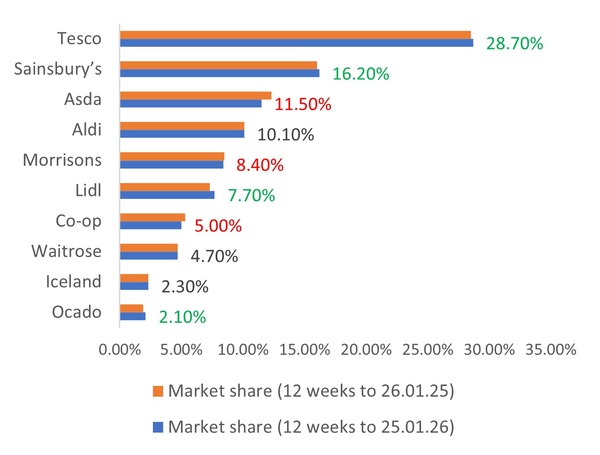

UK Grocery Market Share (12 weeks to 25 January)

Source: Kantar, Retail Economics

Source: Kantar, Retail Economics