UK Electricals Sector Report summary

February 2026

Period covered: Period covered: 04 January - 31 January 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Electricals sales

Electricals sales rose by xx% year-on-year in January, reversing December’s 4.5% decline and marking a return to growth at the start of 2026.

January’s rebound was driven by a combination of clearance pricing, renewed promotional intensity and steady consumer appetite for technology upgrades. Growth was restrained, although the directional shift is notable given the weakness in the lead up to the festive period.

Key drivers and category performance

Retailers extended clearance activity well into January, with price-led campaigns releasing deferred demand from consumers who had postponed purchases during the final months of 2025 in anticipation of stronger deals.

Personal electronics proved particularly resilient. Smartphones, wearable devices and gaming accessories performed steadily, supported by product replacement cycles and gift card redemption. Households used post-Christmas credit and vouchers to upgrade devices, lifting transaction volumes.

Large domestic appliances saw more selective demand. Replacement-driven purchases continued, particularly where breakdowns or energy efficiency considerations justified immediate action. However, aspirational upgrades remained limited, indicating continued caution around big-ticket commitments.

Overall, January’s performance was driven by tactical pricing and product replacement. The appetite for technology remains intact, but purchasing remains value-conscious.

Footfall patterns

Total retail footfall declined year-on-year in January, with weekday visits particularly affected by adverse weather. Electricals retailers experienced softer browsing activity in urban high streets but steadier traffic in retail parks and destination stores.

Digital engagement complemented physical visits, with many customers finalising transactions online after in-store research, or reserving items for collection.

Underlying environment

The macroeconomic environment provided cautious support. Headline inflation eased to 3.0%, its lowest rate in nearly a year, relieving some pressure on household budgets. Wage growth continued to outpace inflation, sustaining real income growth even as labour market conditions softened.

Consumer confidence improved to xx, with households expressing greater optimism about their personal finances than about the wider economy.

Interest rates were held at xx%, and expectations of reductions later in 2026 improved sentiment around future borrowing costs. Electrical purchases are sometimes credit-assisted, particularly for higher-value appliances and technology. Stable rate expectations therefore reduce uncertainty, though borrowing conditions remain tighter than pre-2023 norms.

The labour market showed further signs of cooling, with unemployment edging higher. At the same time, housing market stabilisation supports replacement demand for appliances linked to moves or refurbishments, albeit at modest volumes.

Outlook

January’s rebound provides welcome momentum after December’s contraction. Growth is likely to stabilise as promotional intensity eases. Replacement cycles and innovation in personal technology should continue to support baseline demand, while large appliance sales will remain sensitive to household confidence and housing activity.

The sector enters the spring period in improved shape, supported by stabilising macro conditions and entrenched digital purchasing habits. Sustained progress will depend on product innovation, pricing discipline and consumer confidence building in the months ahead.

Take out a FREE 30 day membership trial to read the full report.

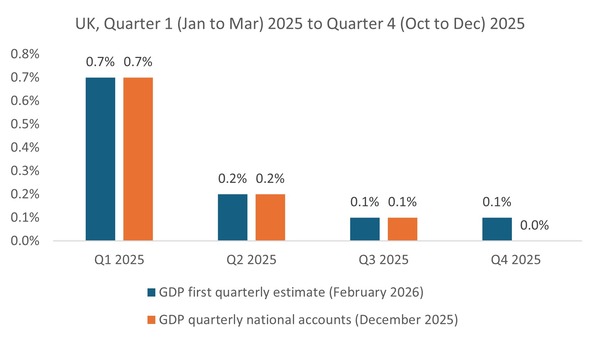

Real GDP is estimated to have increased by 0.1% in Quarter 4 2025

Source: Retail Economics, ONS

Source: Retail Economics, ONS