UK DIY & Gardening Sector Report summary

February 2026

Period covered: Period covered: 04 January - 31 January 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

DIY & Gardening Sales

DIY and gardening sales rose by xx% year-on-year in January, reversing the xx% decline recorded a year earlier and recovering from December’s xx% contraction.

Key trading themes and drivers

Trading was driven by clearance activity and tactical discounting. Retailers used promotions to stimulate demand across tools, decorating supplies and selected home maintenance lines. Shoppers who had deferred purchases in recent months responded to price-led incentives, particularly on practical and maintenance-oriented categories.

Weather influenced category mix. Severe frosts early in the month lifted demand for emergency repair products, insulation materials and heating-related accessories. As conditions deteriorated into heavy rain and storm disruption, outdoor project activity slowed, weighing on core gardening lines and larger improvement works.

Gardening performance was also mixed. Seasonal demand remains limited in January, though sales of indoor plants, early-seed preparations and garden maintenance products provided a degree of support.

Retail parks proved relatively resilient destinations. Their accessibility supported mission-led purchasing, particularly when households required urgent maintenance items following storm damage. Larger format stores benefited from multi-purpose shopping trips, while high street hardware outlets experienced softer footfall during weekday disruption.

Consumers increasingly compared prices and checked stock availability online before committing to store visits.

Overall, January’s growth was functional, with households prioritised maintenance and smaller refresh projects over extensive renovations.

Macroeconomic backdrop

The macroeconomic environment provided incremental support but not a decisive catalyst for the category. Headline inflation eased to xx%, reducing pressure on disposable income. Wage growth remained ahead of inflation, sustaining real income gains and supporting smaller discretionary projects.

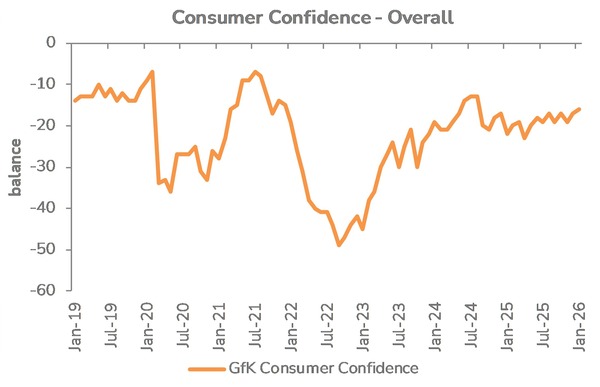

Consumer confidence improved to xx, driven largely by stronger sentiment regarding personal finances.

Interest rates held at xx%, with expectations building for gradual reductions later in 2026. Borrowing conditions therefore remain tighter than historical norms, constraining appetite for debt-financed renovations. For DIY retailers, this continues to limit an acceleration in high-value structural improvement categories.

The housing market showed early signs of stabilisation, with house prices rising month-on-month and returning to annual growth. While transaction volumes remain below long-term averages, the absence of further deterioration supports home-related spending at a replacement and upkeep level.

Labour market softening introduces caution into forward planning, particularly for larger discretionary projects. However, household balance sheets appear more stable than in late 2024, providing a platform for gradual recovery as economic clarity improves.

Outlook

Clearance activity and weather-related maintenance demand provided short-term support in January, but structural improvement activity remains restrained.

As spring approaches, gardening categories should begin to recover seasonally, offering incremental upside. The pace of that recovery will depend on weather stability and a continued easing in inflation. Larger renovation cycles are likely to remain closely tied to housing activity and borrowing conditions.

Take out a FREE 30 day membership trial to read the full report.

Confidence rose by one point to -16 in January

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK