UK DIY & Gardening Sector Report summary

April 2026

Period covered: Period covered: 01 March - 04 April 2026

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30-day membership trial now.

DIY & Gardening Sales

DIY and gardening sales rose by xx% year-on-year in March, an improvement on the xx% decline recorded in February and outperforming the xx% growth seen a year earlier.

The category delivered one of the stronger recoveries across non-food, supported by seasonal demand and favourable trading conditions.

Key trading themes and drivers

The category benefited from a strong start to the month. Warmer and drier weather across much of southern England supported gardening activity, driving demand for outdoor products, plants and garden maintenance.

Seasonal timing played a central role, with consumers engaging with spring-related projects earlier than usual, supported by improved conditions. With Easter falling earlier this year, a portion of demand was brought forward into March, particularly across gardening and outdoor preparation, creating a stronger base for growth that is likely to unwind in April.

As the month progressed, the broader shift in consumer sentiment became more evident. The escalation of conflict in the Middle East led to increased caution in discretionary spending. However, DIY and gardening proved more resilient than other home-related categories.

A key driver of this resilience is the category’s weighting towards repair, maintenance and smaller-scale projects. These purchases are often considered necessary or practical, making them less sensitive to short-term changes in confidence compared with larger home investments.

Kingfisher reported continued strength in UK and Ireland like-for-like sales, supported by trade demand, e-commerce growth and market share gains following competitor exits. The group highlighted that its customer base is more focused on maintenance and improvement which has helped insulate performance.

Macroeconomic backdrop

The macroeconomic backdrop became more uncertain during March, though its impact on DIY and gardening was more limited than in other discretionary categories.

Inflation rose to xx% year-on-year, driven by higher fuel, transport and food costs. These pressures continue to weigh on household budgets, increasing sensitivity to spending.

The escalation of conflict in the Middle East has added to inflationary risk, particularly through higher energy and commodity prices. These pressures are expected to feed through into supply chains and consumer prices over the coming months.

Monetary policy expectations have shifted, with interest rates held at xx% and expectations for rate cuts reduced. Higher borrowing costs are likely to weigh on housing activity and larger renovation projects.

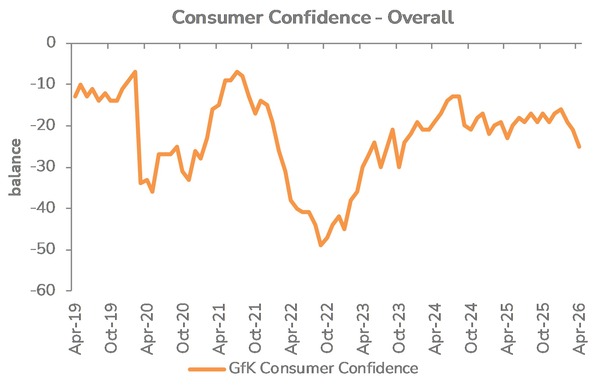

Consumer confidence declined during the month, with households becoming more cautious about the economic outlook. This has led to increased precautionary saving and reduced appetite for major purchases.

Take out a FREE 30 day membership trial to read the full report.

Confidence fell four points to -25 in April

Source: Retail Economics analysis, GFK

Source: Retail Economics analysis, GFK