UK Online Retail Sales Report summary

December 2025

Period covered: Period covered: 02 November - 29 November 2025

3 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Online performance

Online retail sales rose by xx% year-on-year in November (value, non-seasonally adjusted), a sharp turnaround from the xx% decline a year ago.

The timing of Black Friday, which fell outside the comparable period in 2024, significantly boosted growth. All online categories recorded positive year-on-year growth.

Average weekly online sales reached GBP xxm, up from GBP xxm a year earlier, marking the highest weekly total recorded this year.

Online accounted for xx% of all retail sales in November, well above the xx% share recorded in November 2024 and notably higher than the 12-month average.

Key drivers

Black Friday inclusion: Unlike in 2024, this year's November data captured Black Friday (28 November), significantly boosting comparisons. Retailers launched online promotions earlier and more aggressively, leading to elevated sales throughout the month.

Discount-led behaviour: High promotional participation, including widespread use of loyalty discounts and targeted digital offers, incentivised online purchasing.

Our research with MRI Software showed that three quarters of consumers intended to shop during Black Friday.

Convenience and weather: Store-based footfall remained below 2024 levels throughout most of November, with only a short-lived boost on Black Friday itself.

Many shoppers avoided high streets and shopping centres during poor weather, including Storm Claudia mid-month, and turned to online alternatives. This helped accelerate digital sales across categories.

Macroeconomic backdrop

Consumer confidence weakened in November ahead of the Budget, with GfK's index falling to xx. Major purchase intentions also declined, contributing to cautious spending patterns.

Inflation eased to xx% in November, including notable declines in categories like clothing and food. This supported real incomes, though household finances remained under pressure.

Wage growth softened and unemployment edged higher to xx%, but consumer credit use remained contained.

The Bank of England cut interest rates by xx basis points in December following November's sharp inflation drop. While this came too late to influence most November shopping decisions, mortgage lenders had already begun trimming rates, slightly easing pressure on homeowner budgets.

Outlook

While Black Friday timing flattered year-on-year growth in November, the underlying behaviour points to consumers using digital channels to control cost, timing and choice in a still uncertain environment.

Online demand should remain elevated in December, as options such as click and collect absorb late season spending. However, this strength is heavily promotion-led.

Price sensitivity remains high and cost pressures across delivery, returns and fulfilment mean sales growth does not automatically translate into improved financial performance.

The final weeks of the golden quarter will be less about driving additional demand and more about how efficiently existing demand is converted.

Take out a FREE 30 day membership trial to read the full report.

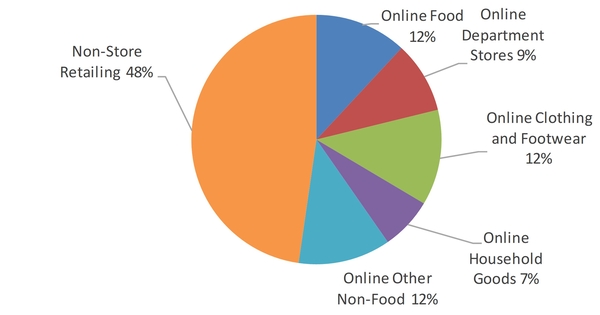

Proportion of online retail sales by category (Period aligned to ONS trading calendar – 2 – 29 November 2025)

Source: ONS, Retail Economics analysis

Source: ONS, Retail Economics analysis