GDP Monthly Estimate: January 2022

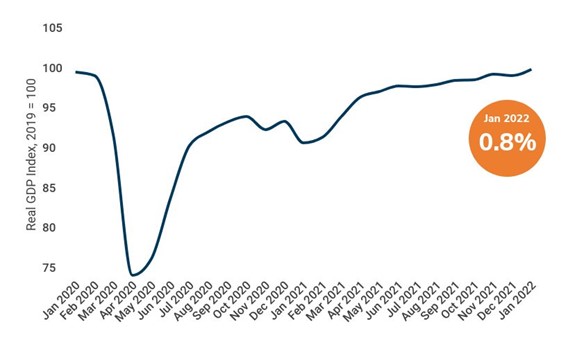

UK GDP grew 0.8% in January, and also 0.8% above February 2020’s pre-pandemic level

Monthly GDP index, January 2020 until January 2022, 2019 = 100. Source: ONS

- GDP bounced back in January, increasing by 0.8% after falling by 0.2% in December, when the Omicron variant and Plan B restrictions had a more significant impact.

- Monthly economic activity is also 0.8% above its pre-pandemic level (Feb 2020).

- All sectors grew in January 2022, with services up 0.8%, production up 0.7% and construction up by 1.1%.

Services

Services grew 0.8% in January and is now 1.3% above its pre-pandemic level (Feb 2020). This followed a 0.5% fall in December.

Sectors that were hit particularly hard by the Omicron variant in December recovered in January, including wholesaling, retail and restaurants which all performed strongly.

Consumer-facing services grew by 1.7% in January, driven by 6.8% growth in food and beverage service activities (following a fall of 8.1% in December). Dining out and socialising proved popular in January after many limited social contact in the run up to Christmas due to Omicron concerns.

Wholesale and retail trade grew by 2.5% in January and was the main contributor to services growth. Information and communication was the second largest contributor to the growth in services, which grew by 2.9%. Computer programming and related activities grew by 6.5%, while film and tv production, sound recording and music publishing activities grew by 6.7%.

Overall, services output grew by 1.0% in the three months to January, compared with the previous three months (Aug-Oct). Consumer-facing services were 6.8% below their pre-pandemic levels (Feb 2020), while all other services are 3.4% above them.

Construction

Construction output increased 1.1% in January, following a rise of 2.0% in December. This is the third consecutive monthly growth greater than 1.0% with the construction sector now 1.4% above Feb 2020’s pre-pandemic level.

The increase in monthly construction output in January was driven by an increase in repair and maintenance (4.6%) while new work saw a decline of 0.8%.

Anecdotal evidence suggests some of the issues in sourcing construction products in the latter half of 2021 has continued to ease. Alongside this, new orders in the construction industry continued to perform strongly, growing by 9.2% in Q4 2021 compared with Q3.

Overall, in the three months to January, construction output increased by 3.0%.

Production

Production output increased by 0.7% in January, following growth of 0.3% in December.

Manufacturing (0.8%) was the primary growth driver in January. Growth in manufacturing was widespread with increases in 10 out of the 13 sub-sectors, partially offset by falls of 23.3% in the manufacture of pharmaceutical products and of 4.5% in the manufacture of transport equipment both of which increased strongly in December 2021.

However, production output remains 2.0% below its February 2020 level, the last month of “normal” trading conditions prior to the pandemic, with manufacturing sitting 1.6% below.

Overall, in the three months to January, production output rose by 0.4%, with growth of 0.8% in manufacturing, 1.0% in electricity, gas, steam and air conditioning supply, and 2.6% in water supply and sewerage. This was partially offset by a decrease of 8.3% in mining and quarrying.

GDP Sector Breakdown

Source: ONS

Back to Retail Economic News