UK Retail Economic Briefing Report summary

November 2021

Period covered: Period covered: November 2021

1 minute read

Note: This report summary is one or two months behind the current month as standard reporting practice. The content is indicative only and incomplete with certain data undisclosed. Become a member to access this data or take out a free 30 day membership trial now.

Economic activity

The UK’s economic recovery slowed between July and September, as supply chain disruption and labour shortages held back growth.

GDP rose by an estimated 1.3% in Q3 2021. This represents a marked slowdown on the 5.5% increase seen in Q2. UK GDP is forecast to grow by 00% in 2021 and 00% in 2022

Confidence

GfK’s Consumer Confidence score rose by three points to 00 % in November – recovering some lost ground after falling sharply in October.

Business confidence is wobbling however. Only 00 % of UK CFOs are more optimistic about the financial prospects of their company compared to three months ago, down from 54% in Q2 2021.

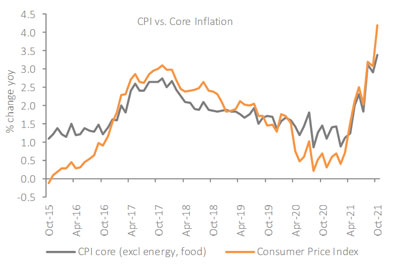

Inflation

CPI inflation jumped 00% YoY in October, up from 3.1% last month. This reflected the increase in the energy price cap on 1 October following record rises in energy prices after economies emerged from lockdowns.

Retail Economics research shows that 00% of UK consumers are worried about rising living costs, up from 54% in September.

Labour Market

The labour market has outperformed expectations following the end of the furlough scheme on 30 September.

The unemployment rate in the UK edged down to 00% in the three months to September, from 4.5% previously. This is 0.3 percentage points (pp) higher than before the pandemic.

Between August and October, the number of vacancies rose to new record highs, reaching 0,000,000 – some 388,000 above its pre-pandemic Q1 2020 level.

Take out a FREE 30 day membership trial to read the full report.

Inflation rising sharply

Source: ONS

Source: ONS