UK DIY & Gardening Sector Report summary

January 2021

Period covered: Period covered: 29 November 2020 – 02 January 2021

Retail sales rose by 0.8% in December, year-on-year, according to Retail Economics. Total online retail sales rocketed by 45.8% in December, value and non-seasonally adjusted, according to ONS. Shop price inflation fell by 0.6% in December, excluding fuel, according to ONS. DIY & Gardening retail sales rose by 12.5% in December, year-on-year, value and non-seasonally adjusted, according to Retail Economics. Average weekly sales for DIY & Gardening were £148m in December, according to Retail Economics.

DIY and Gardening – December 2020

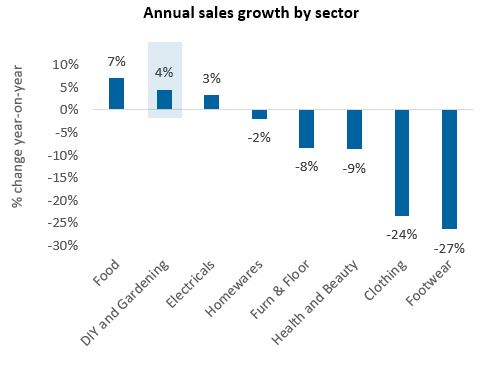

DIY & Gardening remained the strongest performing category in December, with sales growth rising by 12.5% in December, year-on-year. This was against a weak comparison a year ago when sales growth fell by 3.0%. Stronger performances in recent months meant that sales growth underperformed the three-month average of 13.7% but remained comfortably above the 12-month rolling average.

Christmas trading period

The traditional pattern of Christmas consumer spending was disrupted by the national lockdown in November and introduction of a new tiered system for coronavirus restrictions at the beginning of December. Our own analysis suggested that some consumers brought forward their Christmas shopping into the November trading period with over half of consumers (53%) indicating at the start of December that they had completed more of their Christmas shopping.

Looking ahead

The strong momentum of sales growth is likely to be carried into 2021. The recent announcement that current coronavirus restrictions were only beginning to be lifted from 8 March, indicates consumers will be spending more time at home than previously intended. This could create a new wave of ‘DIYers’ looking to complete projects before life returns to normal.

Macro Factors – Housing Market Activity

Mortgage approvals accelerated further in November to 104,969 up from 98,338 in the previous month and significantly ahead of the previous six-month average of 65,733. It was the sharpest rise in approvals since August 2007. Notably, mortgage approvals in the 11 months to November 2020 are broadly in line with the corresponding period in 2019 and are up by 61% compared to the same month a year ago. The number of re-mortgaging approvals edged up, totalling 35,107 in November up from 33,089 in… read more

Macro Factors – Consumers

Household consumption rose by 19.5% in the third quarter of 2020. The main drivers were increased spending in restaurants and hotels, and transport. Household consumption remains 9.8% below its Q4 2019 level. GfK’s Consumer Confidence measure improved by seven points to -26 in December, this is 11 points lower than a year ago.

Macro Factors – Ipsos Retail Performance

Footfall fell by 53.7% in December 2020 year-on-year, according to latest figures from Ipsos Retail Performance (which measures footfall in over 4,000 non-food stores across the country). The steepest declines in footfall for the month of December were in London & South East (-61.9%) followed by Scotland & N Ireland (59.2%) and The Midlands (-52.1%). Similarly, footfall fell in SW England & Wales (-50.9%) and Northern England (-44.8%).

Macro Factors – Labour Market

The latest ONS labour market data shows a significant increase in unemployment rate while employment rate continues to fall. Though redundancy levels reached record highs, total hours worked increased from the low levels in the previous quarter. The number of paid employees fell by 2.7%, some 828,000 employees in December compared with February 2020 according to flash estimates using PAYE data – around 52,000 higher than in… read more

Macro Factors – Earnings

For November in nominal terms (unadjusted for price inflation): Average regular pay (excluding bonuses) for employees in Great Britain was £531 per week before tax and other deductions from pay – up from £510 per week a year earlier. Average totals pay (including bonuses) for employees in Great Britain was £562 per week before tax and other deductions from pay.

Macro Factors – Costs, Prices and Margins

Sterling’s trade weighted index dipped marginally in December, down 0.3% on the previous month as Brexit uncertainty and rising coronavirus cases impacted the index. In terms of exchange rates, the £/$ rate is currently around 1.36, while £/€ rose to around 1.12. Both commodity indexes we track appreciated in January. Indeed, the Thomson Reuters CRB Index fell by 3.9% year -on -year from -11.9% in December, compared to a 17.6% annual fall for the GSCI Commodities benchmark. The rise was driven by expectations of strong international demand during 2021.

Factory gate inflation (output) slowed in December, rising to -0.4% year-on-year from -0.6% in November. On a month-on-month basis, output inflation rose by 0.3%, unchanged from the previous month. Two product groups provided a negative contribution to the annual output inflation rate in December. Indeed, Petroleum provided the largest downward contribution of 1.53 percentage points (pp) to the annual output rate, with inflation falling by 26.6% year-on-year, driven by refined petroleum products. Paper and printing products displayed the second-largest downward… read more

The year of home improvements

Source: Source: Retail Economics index

Source: Source: Retail Economics index